Shipping Market Outlook – 1Q2013

As part of my job at ExxonMobil, I was in charge (among other things) of providing a concise quarterly update on the state of shipping markets and their outlook for the medium term. This information was gathered from various shipping intelligence sources, such as Lloyd’s Marine Intelligence Unit, Clarkson’s, Alphaliner, Alphatanker, Tradewinds Newspaper, and other databases. The intelligence I compiled was distributed across ExxonMobil’s marine departments in order to insure the underlying economic conditions our customers were operating in were understood.

The presentation was done under PowerPoint format, so I am providing a brief explanation of the content under each posted slide. The material is quite complex for someone unfamiliar with shipping economics so please feel free to contact me. I would be more than happy to clarify/explain the content.

Four general underlying factors were affecting the state of shipping markets in early 2013

1. Uncertain Demand for Shipping

Since this is directly correlated to growth of trade and thus global economic output, the slow emergence from the financial crisis – compounded by the Euro crisis in Europe, slowdown in Asia, and geopolitical volatility in the Middle East – means uncertain times for demand for shipping moving forward.

2. Ship Oversupply

The second and perhaps most important factor is a large oversupply of vessels due to excessive orders during the bull market prior to the 2009 crisis. Ships take on average two to three years between order and delivery, and new tonnage keeps hitting the water, further putting downward pressure on freight rates companies are able to charge.

3. Price of bunker fuel

With 40% of a ship’s operating expenses being bunker fuel, the fact that the price of oil is creeping upwards is putting further pressure on players who are already struggling with the very low freight rates.

4. Lack of new financing

Banks are less willing to lend and refinance shipping companies as they become riskier and riskier and offer lower returns.

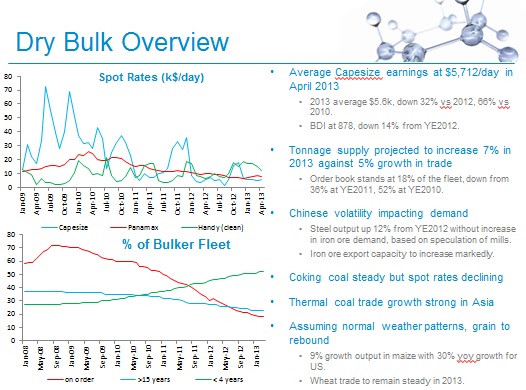

Above are some details about the dry bulk market (vessels that carry “dry” products, ie ore, wood, grain, etc.) which comprise about 40% of the 10,000 commercial vessel fleet worldwide.

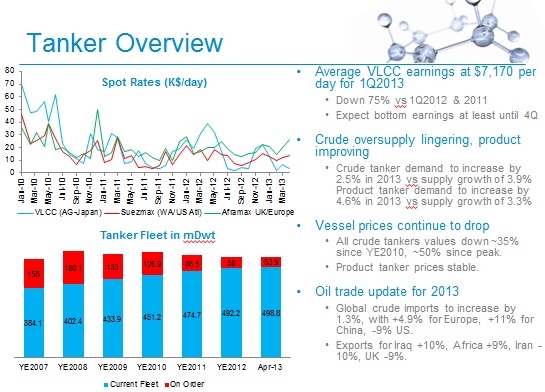

Above are some details about the tanker market (vessels that carry liquid products, ie oil, liquefied gas, chemicals, etc.) which comprise about 30% of the 10,000 commercial vessel fleet worldwide.

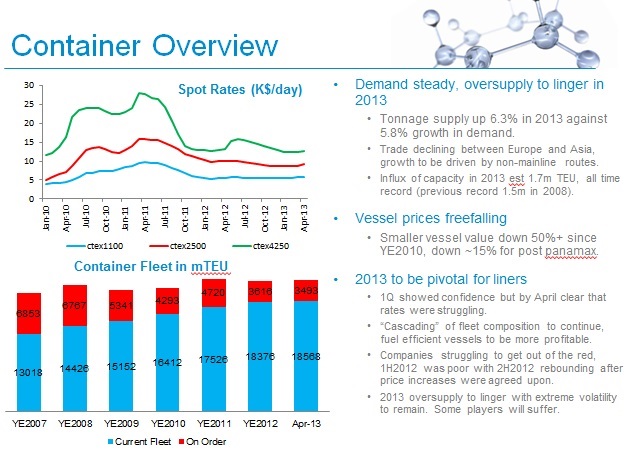

Above are some details about the container market (vessels that carry standardized containers containing a wide array of products) which comprise about 15% of the 10,000 commercial vessel fleet worldwide.

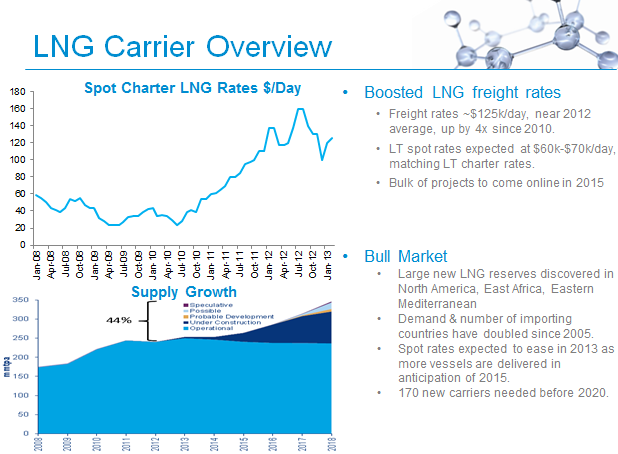

Above are some details about the LNG market (highly specialized vessels which carry liquefied natural gas). It is a sub segment of tankers and is currently a booming market.

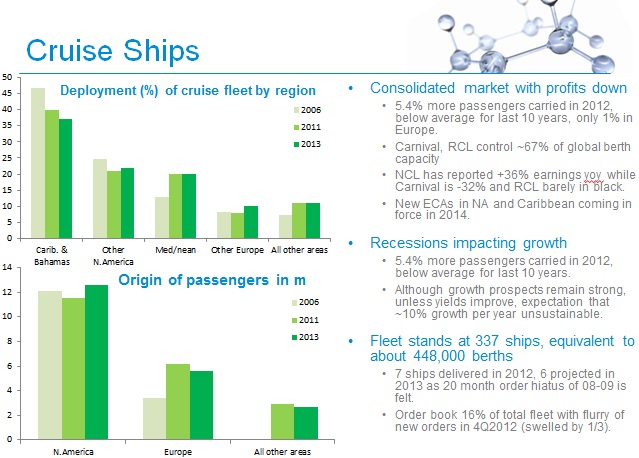

Above are some details about the cruise market (vessels carrying passengers for leisure purposes).

A summary of the shipping segments and their current outlook.

A summary of the shipping segments and their current outlook.