Let’s start with the basics. Developed in 2009 by an anonymous group known as Satoshi Nakamoto, a blockchain is a highly encrypted and shared database which facilitates transactions in the form of digital cryptocurrencies such as Bitcoin. This technology aims to provide a secure and faster way to digitally and anonymously send payments between two parties without needing a third party to verify the transaction. It also provides a tamper-proof alternative to tedious banking processes that are “typically bureaucratic, time-consuming, paper-heavy, and expensive.” (Meola, A., 2017).

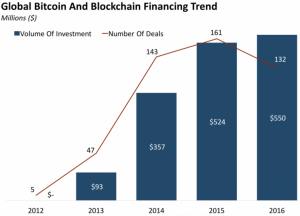

Since its birth in 2009, the number bitcoin transactions have skyrocketed, as seen in Figure 1. In addition, the value of each bitcoin has risen from US$1 to roughly $1,100 today (E., 2014).

Figure 1. Source: Business Insider

The credit for this rapid success goes to the numerous benefits provided by bitcoin. Firstly, it eliminates the need for a third party, which reduces transaction costs to a bare minimum of 1% or even free through some bitcoin gateways, compared to an average of 3-4% on credit card purchases. In addition, businesses receive money in hand the day after the transaction instead of usually having to wait 3-5 business days, hence greatly improving their cash flow (E., 2014).

Bitcoins are now being used to buy food, ebooks, music etc. Secondly, the blockchain server on which bitcoins operate provides complete transparency to users who can log in and browse through every single bitcoin transaction ever made (E., 2014).

In his famous blog titled “Both sides”, the American entrepreneur Mark Suster provides valuable insights into the world of blockchains, stretching even further than cryptocurrency. He mentioned that the strongly encrypted algorithms used in a blockchain can, in fact, be used to transfer confidential paperwork between large businesses as well as governments, ensuring that data isn’t tampered in any form.

He has also shown concerns about the reliability of bitcoins stating that, it’s increased valuation is all because of high speculation and a drive for quick profit which is highly unstable and may not be sustainable in the long run.

Additional concerns with bitcoin include it’s safety. In 2014, 800,000 bitcoins valued at $450 million were lost at a Japanese bitcoin exchange called ‘Mt.Gox’. Furthermore, the federal government is concerned that it might soon be used for terrorism purposes (E., 2014).

In conclusion, I personally think that bitcoins are not a reliable option to replace currency because of the aforementioned reasons as well as the fact that its origin is anonymous even today and there is no central body to govern it and responsible for anything that might go wrong with it.

However, I do believe that the blockchain technology could be applied in other fields like secure document sharing which could be greatly beneficial to governments and businesses across the globe.

Works Cited:

E. (2014, May 29). Retrieved October 15, 2017, from https://www.youtube.com/watch?v=SmExLsqQYEw&t=325s.

Meola, A. (2017, August 25). Understanding blockchain technology, bitcoins and the rise of cryptocurrency. Retrieved October 15, 2017, from http://www.businessinsider.com/blockchain-technology-cryptocurrency-explained-2017-8

Suster, M. (2017, September 18). Want to Really Understand What all the Hype of Cryptocurrency is About? Retrieved October 15, 2017, from https://bothsidesofthetable.com/the-case-for-against-cryptocurrencies-101-c8d71c444fe0