Just a few days ago, the CEO of Amazon Jeff Bezos, became the richest person in the world with a net worth of $93.1 Billion, a $3.1 billion margin over Bill Gates. In recent years, Amazon is recognized for its bold moves to expand: a $13.4 billion acquisition over Whole Food Market as a way to increase its online sales, Amazon Prime Air which allows drone – instead of human – deliver your online shopping goods at a much efficient rate to your living space, and just a week ago its announcement of Amazon key, which let Amazon staff to unlock your front door to deliver your package or even to offer house cleaning services. From an investor perspective, this massive conglomerate giant seems to want every piece of opportunities, which diversifies its risks but also attracts bigger competition at the same time. Other potential worries also include anti-trust action: what if Amazon becomes an e-commerce monopoly in the near future? These audacious acts reflect Amazon’s goal to expand globally and to position themselves in the new market. In this blog, I would like to emphasize the value of thinking long-term.

Figure 1.1. Statistics of Amazon’s Revenue and Net Income from 1997 to 2015.

Figure 1.1. Statistics of Amazon’s Revenue and Net Income from 1997 to 2015.

In a business era where Investors focuses on short-term results, Amazon plays its game long-term. Jeff Bezos once said that its ultimate goal (or BHAG) is to make it ‘irresponsible’ to not be a Prime Member. On the surface, Amazon has already achieved at satisfying customer needs: an online engine that offers a bucket list of items. Below the surface, they are investing in new technology (20% more than Google), opening new warehouses as a way to expand its distribution channels, dumping a 5$ million investment in India for digital payment technology, and so on. However, Instead of setting growth goals quarter by quarter, Amazon plays it much more slowly but ambitious. Every strategic initiative is not a move to merely generate profits so that they can receive more funds from the investor, but a potentially revolutionary change to the existing environment. Not only are these moves long-term oriented, but they are also creating a loyalty cycle: every strategic expansion Amazon purses are in support of its BHAG of making a consumer more willing to purchase Amazon Prime Membership. From a value proposition perspective, Amazon’s long-term oriented moves are transforming their business model into an infrastructure of the massive marketplace, from e-commerce, payment and finally to logistics. Although this strategy may require Amazon to invest more times in R&D, every piece of Amazon’s technologies will become part of their comparative advantage.

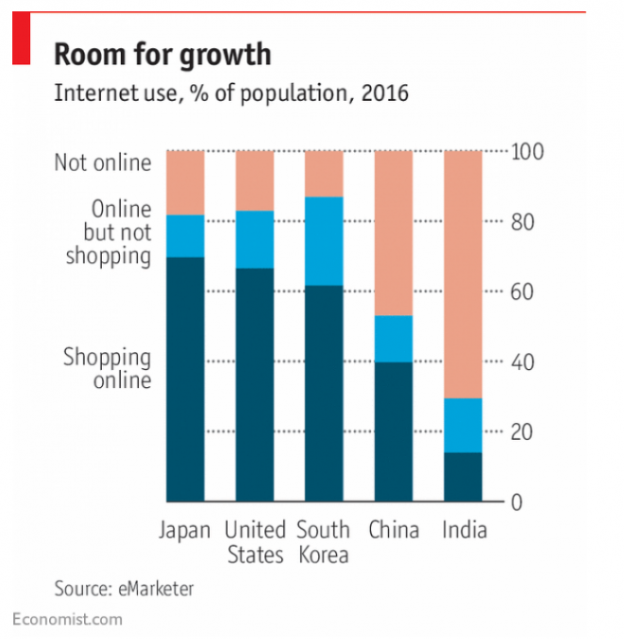

While Amazon has already established itself as the fifth most valuable company, most investors believe Amazon’s value will increase even more as the room for growth is still huge.

Figure 1.2. Room for internet uses growth 2016.

Figure 1.2. Room for internet uses growth 2016.

Word counts: 450

Bibliography

Reuters, T. (2017, October 26). Amazon sales surge after Whole Foods acquisition, busy Prime Day. Retrieved October 29, 2017, from http://www.cbc.ca/news/business/amazon-earnings-1.4374005

Vinton, K. (2017, October 27). Bezos’ $10 Billion Day Boosts Net Worth To Record High, Cements Him As No. 1. Retrieved October 29, 2017, from https://www.forbes.com/sites/katevinton/2017/10/27/bezos-10-billion-day-boosts-net-worth-to-record-high-cements-him-as-no-1/#5f81c980454e

Why investors are so keen on Amazon. (2017, April 03). Retrieved October 29, 2017, from https://www.economist.com/blogs/economist-explains/2017/04/economist-explains

Alibaba and Amazon look to go global. (2017, October 28). Retrieved October 29, 2017, from https://www.economist.com/news/special-report/21730539-e-commerce-giants-are-trying-export-their-success-alibaba-and-amazon-look-go-global