Authors note: This blog was written for FRE528: Environmental Economics and Policy

I often find the best way to dig into a fisheries management policy is to start with two blank pieces of paper, one for a list of acronyms, the other for a jurisdiction flow chart. There’s nothing that bureaucrats love more than filling their documents with these codes, and wrapping your head around what they’re really talking about can be challenging, to say the least. So here’s the acronyms you’ll need for the next 1200 words:

ASMFC: Atlantic States Marine Fisheries Commission

FMP: Fisheries Management Plan

LEC: Law Enforcement Committee

MCS: Monitoring, Control and Surveillance

MSY: Maximum Sustainable Yield

NMFS: National Marine Fisheries Service

NOAA: National Oceanic and Atmospheric Administration

RFMC: Regional Fisheries Management Council

TAC: Total Allowable Catch

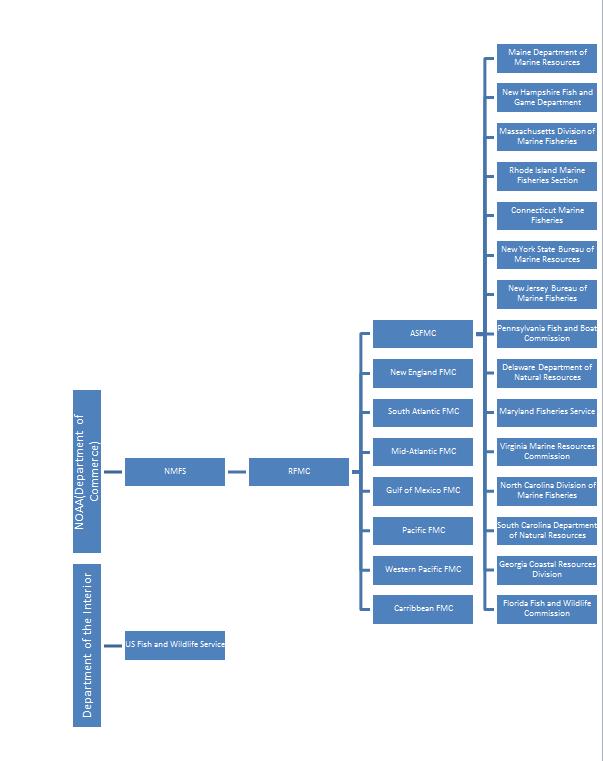

Whew, that’s a lot of jargon. Here’s the jurisdictional flow chart:

What’s important for understanding US fisheries policy is that there are lots of different national and state level departments either working together or at odds with each other and they’re all trying to manage these resources that do not stay within state lines, darn fishes! As President Obama mentioned in his 2011 State of the Union Address, “The Interior Department is in charge of salmon while they’re in fresh water, but the Commerce Department handles them when they’re in salt water,” the President continued with a classic dad-joke, “I hear it gets even more complicated once their smoked,” (which is probably true).

The reason why NOAA sits in the Department of Commerce and not in the Department of the Interior could be chalked up the role of marine fisheries in the economy, or the nature of shipping in ocean waters or even how important weather is to business, but really Nixon was just mad at the Secretary of the Interior when NOAA was formed in 1970, and so plopped it in Commerce. And so it goes with much government management – often it is more based on personal relationships than any overarching political or economic theory.

Within NOAA, there are lots of other departments, like the National Weather Service, the National Ocean Service and the National Geodetic Survey. The office that manages the nation’s fisheries is the appropriately named National Marine Fisheries Service (NMFS). NMFS does a lot of their own management and research, but a lot of the FMP’s are left to the RFMC’s (see, isn’t that acronym list coming in handy now?). There are eight RFMCs, the idea being that regional fisheries management can respond better to stakeholders needs. The RFMC that we’re slowly narrowing in on for this assignment is the ASMFC, made up of the 15 states of the Eastern seaboard. Each state commission’s three members to the ASMFC, and these individuals are then responsible for creating policy and managing the fisheries within these waters. But wait it’s not that simple- one of the three members is the head of the State marine fisheries agency, meaning that there is also a State agency overseeing these marine resources. Ah the complexity of representative government.

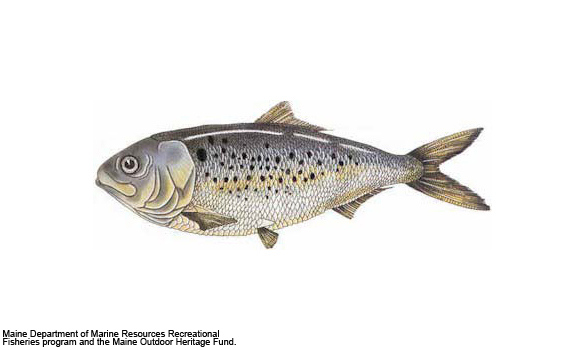

And so finally, at word 503, we get to introduce the star of this blog post, the Menhaden- one of the 25 species the ASMFC manages.

The Menhaden has always been one of my favorite fish, ever since reading Bruce Franklin’s wonderful book: “The Most Important Fish in the Sea: Menhaden and America.” They’re small fish, and they swim with their mouths gaped open, catching algae and phytoplankton as they swim. By doing this, one fish filters up to three gallons of water per minute, playing a crucial role in cleaning the water column. They are also the only forage fish in the Chesapeake and so they take the important role of keystone species, connecting the trophic levels between primary producers and tertiary consumers. Menhaden are important prey for fish we like to eat- like Stripped Bass- and also for birds we like to look at like Ospreys. We don’t eat menhaden; they’re quite smelly due to their high concentration of oil, but that oil makes them perfect for the Omega-3 fatty acid pills that Americans are so fond of. They’re also used for bait in other marine fisheries, both commercial and recreational, and they’re used for fertilizer and feed as fishmeal. All in all, menhaden make up the largest fishery on the East coast, and the second largest in the country (by volume).

What is also amazing about this fishery is that there are only 8 boats involved, all owned by one company-Omega Protein (NYSE: OME). There is another menhaden fishery in the Gulf of Mexico which is larger, but still 90% of the vessels are owned by Omega. Omega vessels use purse seines which cause virtually no bycatch, and the company uses spotter planes to find large schools of menhaden close to the surface. Their incredibly efficient operation harvests 300,000-400,000 metric tons of menhaden annually.

Omega argues that they’ve been fishing menhaden for 100 years without any environmental problems, but scientists disagree. Recent stock assessments show that the population is at a record low, at less than 10% of the historic levels, and that while the stock is not classified as overfished, overfishing has occurred in 32 out of the past 54 years[1] (PEW Environment, 2014). The effects of the population decline are evident in the predators- striped bass, a $6.9 billion fishery in its own right, have shown signs of stress and malnutrition potentially due to the decline in menhaden (ibid).

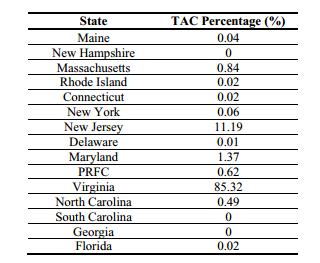

In response to concerns about the population, the ASMFC lowered the TAC in 2012 to 170,800 million tons, a 20% reduction of the 2011 catch (www.asmfc.org). The TAC is allocated at the state level, and then states are required to close the fishery after their TAC has been fished. If the TAC is exceeded, the balance is removed from the next year of the state’s allocation. States are also allowed to trade or combine their TACs. But as you can see from the table below, most of the TAC is assigned to Virginia, not surprisingly, home of the Omega Protein factories.

Enforcement is the state’s responsibility, and can be implemented through on board observers or general MCS of the fishery. The ASMFC has a Law Enforcement Committee (LEC) which is comprised of members of the NOAA Office of Law Enforcement, Coast Guard, and the US Fish and Wildlife Service.

To answer the final checkpoints- the advantages of a TAC is that it caps the amount of fish, and because there’s only one company the TAC does not incentivize increased effort by the fleet. There is no impact on discarding because the fishery has a low rate of bycatch. The TAC is effective in reducing the catch, but whether the reduction is enough to help restore the stock is still a question to be answered.

The menhaden is the most important fish you’ve never heard of, and its management structure outlines the complexity and bureaucracy (bureau-CRAZY) of national fisheries management. In the coming years, increased efforts to understand the ecosystem interactions of the fish will hopefully help to create a stronger, more sustainable management system- based in science and buoyed by economics.

References:

www.asmfc.org: Atlantic States Marine Fisheries Commission

Hank Shultz. Nutraingredients-usa.com. Dec 19, 2012 “Omega Protein’s Atlantic menhaden catch to be cut by 20%” http://www.nutraingredients-usa.com/Suppliers2/Omega-Protein-s-Atlantic-menhaden-catch-to-be-cut-by-20

Atlantic Menhaden Campaign. http://www.pewenvironment.org/campaigns/atlantic-menhaden-campaign/id/85899364506

[1] There’s also an important difference in the language used to describe fisheries- “overfished” means that the overall biomass of a stock is depleted, while “overfishing” occurs when annual fishing effort is greater than the MSY.