London congestion charge

London’s traffic system has a notorious fame around the world. But can merely rely on the economic theory to charge on the congestion problem can solve it?

Normally, the economic theory can only applied in the optimal situations; any externalities or uncontrolled factors could ruin the idea.

However, there are more than one cities are implementing the charge on traffic, such as Singapore, Olso and Bergen in Norway[1]. So in this blog, I will introduce what is this charge, what’s it coverage and how it works.

The congestion charge is summarized as below:

| Year of policy | Charging time | Charge amount |

| 2003.Feb.17-2005 | 7:00am-8:30pm | 5 pounds |

| 2005.July- | 7:00am-8:30pm | 8 pounds |

During the weekdays of charging time, whenever you enter into the charging area, which located in the central of London, you have to pay such amount of money, excluding exempted vehicles. Payment was made convenient to citizen, can be paid either by phone, Internet or buy the charge fee in an outlet. Thinking of how to escape from it? No way, city was spread with cameras, the vehicle plate number will be taken by the camera and compare with system of paid list. Motorists who haven’t pay will face a fine as high as 120 pounds.

This policy was expected to generate a revenue of 100 million pounds per year.

Effectiveness:

It is reported that this policy has largely increased the traffic speeds. Average traffic speed during the charge days (weekdays) has increased 37%. Peak hour congestions has decreased 30% and bus congestion delays has decreased around 50%. Bus ridership increased 14% and subway ridership increased 1%. Overall amount of transport in London has decreased during the past years around 21%, which equal to 70,000 vehicles. According to the source from Transport in London.[2] .

The statistics shows positive signs of the effectiveness of this policy scheme. There are also counter points that prove congestion charge does not necessarily works. Despite few cars, according to the statistics, congestion rose significantly during 2005-2006. And average traffic speeds in central London falls from 10.6mph in 2003 to 7,1 mph in 2006.

Although it was justified by the reason such as city fundamental facilities [3]constructions: such water and gas mains replacement. It raises the doubt in its effectiveness..

Nevertheless, there are ways to increase the effectiveness of this policy. For example: we can differentiate the charges by the miles driven, and areas you are in and time that vehicles in the city Centre. Also, citizen’s transit option has been limited in some degree; London should provide a better substitution, such as the bus and subway. However, according to my friend in London, in certain area, he can walk faster than taking a subway. Revenues of the policy should be used to upgrade the public transportation to reduce the externalities caused by this policy.

Drawbacks of the charge:

- Consumers may consider it as a suspicious charge. No one is willing to pay extra and living under the control of the surveillance camera.

- This policy may reduce the social welfare in the way that it reduced the retail revenues of downtown, according to London Chamber of Commerce[4]. In the survey of 2003, the small retailers blamed this policy as the reason of recession of their business. And over time, the small retailers may consider moving out of the Center area.

- No differentiate in the charging in aspect of rich people and poor.

- No differentiate of charges in the time, area, and miles of driven. With these factors into consideration, congestion charge policy could be more effective.

Advantage of policy:

- Create revenue for public transportation upgrading.

- Decreased the overall motors on the street of congested area and furthermore reduce the pollution.

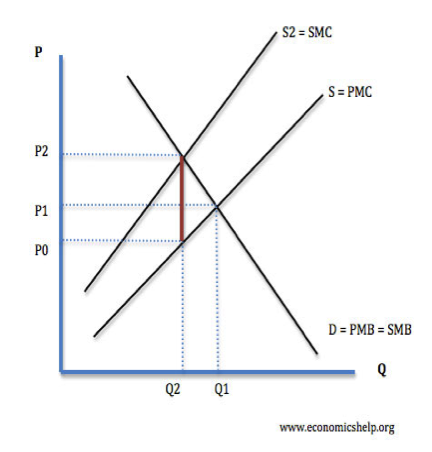

- Put a price on the externalities of the congestion. According to Pettinger (2011)[5] Social cost of congestion is estimated as 20 billion pounds a year. It fixed the problem that petrol tax which cannot differentiate the portion of driving contribute to the congestion[6].

Analysis of the possibility to duplicate

There are certain qualities that a city should have to adopt this policy.

- A city with circle routes, so that driver can choose other ways to circle around the charging area.

- This policy requires large investment in research, installing and operation, so city with a smaller scale may not affordable.

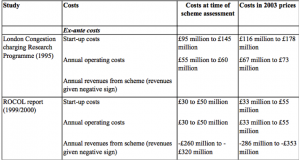

Image retrieve from website[7]:

- City should have other transport options. So that the policy won’t create unnecessary inconvenient to citizens which constitute another externalities.

- This policy requires large investment in research, installing and operation, so city with a smaller scale may not affordable.

-

The education level of the citizen should also be a precondition of the policy, So that the facilities won’t be wrecked frequently. It seemed ridiculous, but from personal experience. This is really a serious aspect should be considered.

[1] http://www.vtpi.org/london.pdf

[2] http://www.tfl.gov.uk/tfl/cclondon/pdfs/ThirdAnnualReportFinal.pdf

[3] http://www.independent.co.uk/news/uk/home-news/the-big-question-has-the-congestion-charge-been-effective-in-reducing-londons-traffic-781505.html

[4] www.londonchamber.co.uk

[5] http://www.economicshelp.org/blog/143/transport/how-effective-is-a-congestion-charge/

[6] http://www.economicshelp.org/blog/143/transport/how-effective-is-a-congestion-charge/

[7] http://www.google.ca/url?sa=t&rct=j&q=london%20%20congestion%20charge%20detailed%20assessment%20&source=web&cd=1&cad=rja&ved=0CC4QFjAA&url=http%3A%2F%2Fuk-air.defra.gov.uk%2Freports%2Fcat09%2F0505171128_London_Congestion_Charge_Detailed_Assessment.doc&ei=rQZNUdWsKavPigKU9YHABA&usg=AFQjCNHlBvPnTCDJfy2OlC8OBhXQKdfHjQ&sig2=98KXUcF0mas9Z1dwZEoijg&bvm=bv.44158598,d.cGE

{kind=link}