Week one was a great learning experience. My understanding of agricultural commodity markets has already grown immensely since we began trading. Despite having read and watched countless tutorials on futures trading prior to the MFRE program, it is clear the futures market is something best learned by doing. Over the past two weeks I have began to develop a rational process when choosing how to position myself in the futures market. My process includes the review of reliable sources and determining their validity by comparing their predictions to daily market trends.

Feeling more confident, I went into week two feeling ready to further my cash exposure to the futures market.

{kind=link}

Week 2:

Week 2 started with a review of my ‘go-to’ online resources (see below). In general I was able to conclude the big events of the prior two weeks (USDA Crop Report & the Fed’s decision) were now fully realized into current commodity prices. I was left with the task to determine what factors will be driving this weeks fluctuations.

Wheat

An article published by Agrimoney.com (http://tinyurl.com/kqljlgt) speculated increases in demand for American origin wheat will limit and potentially reverse the downward trend that was being experienced by wheat prices. This information was enough to justify covering my short and even going long on December wheat futures. As the week progressed my decision to go long proved profitable as further data supported increasing demand for US wheat, encouraging to further my long position by another 5 contracts. Over week two I have been enjoying the slow and steady upward trend experienced by wheat demonstrated below.

(click images to enlarge)

Corn

Unfortunately my successes with wheat did not transpire with corn. Going the hunch that corn may follow the upswing demonstrated by wheat and the , I furthered my existing long position in corn by 13 contracts. To my surprise my hunch was partially correct, on Wednesday, corn experienced a dramatic increase during Wednesday, however, also to my surprise, by the time my order went through, the price of corn was at 4.56/bu, pretty much at the high experienced late Wednesday. Today corn is at 4.53/bu…… Had I placed my order only hours before my corn story would be different. I will be looking out for some new information regarding corn over the weekend so I can reevaluate my position Monday morning.

(click images to enlarge)

Soybeans

I decided to leave my short on soybeans as is. It was a mistake. Soybeans experienced some incredible gains throughout the week. At least I didn’t further my short on soybeans.

(click images to enlarge)

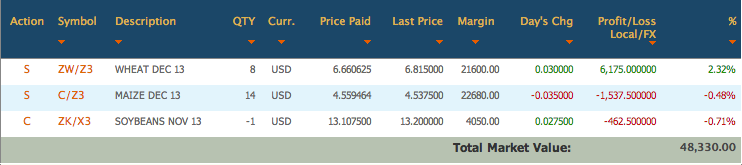

Portfolio Summary

(click images to enlarge)

Conclusions

As mentioned above, I feel my understanding of the commodity markets is growing. That being said, there is absolutely no way I would start investing my own money into trading futures. The difficulty and riskiness of betting on commodity prices explains why investors refer to price swings as bears and bulls rather than bunnies and butterflies. To better my performance next week, I plan to monitor the markets more frequently and earlier in the day in order to take advantage of daily highs and lows.

Resources:

http://www.grainews.ca/

http://www.agrimoney.com/1/commodities/