London Congestion Charge: Policy Overview and Discussion

Policy Overview

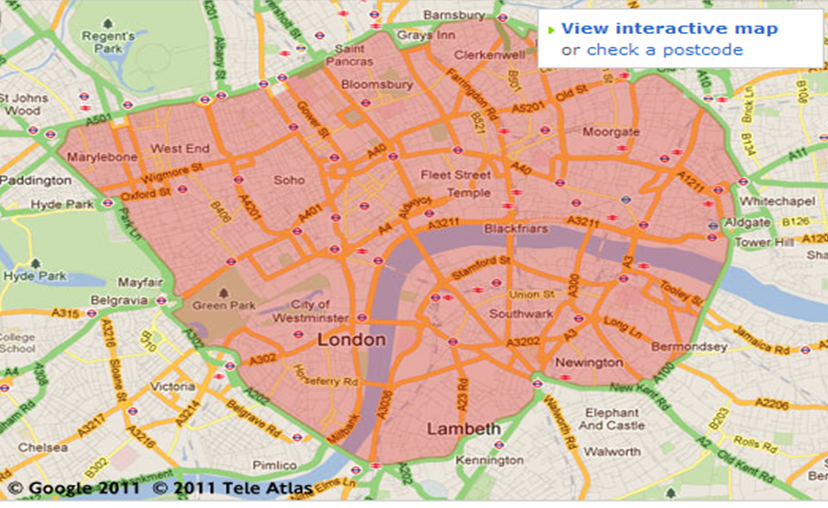

Traffic congestion is a common big issue in most of “big” cities and international cities with highly developing speed. The negative impacts of the traffic congestions, such as lower efficiency, longer waiting queue, increasing fuel wasting and air pollution, etc., and how to control traffic congestions are heated discussed in academic research during the past decade. United Kingdom, one of the developed countries levy congestion charge, published a UK government sponsored document in February 2003 to public that the government introduced the London Congestion Charge (LCC) in the Congestion Charge Zone (CCZ) (Fig.1) in central London, and the Department for Transport would take this responsibility, and stated that their goal of this congestion charge is to improve the traffic efficiency in London and increase the investment supporting for London’s transport system.Fig.1 Map of CCZ – 2011

*Source:TFL” http://www.tfl.gov.uk/tfl/roadusers/congestioncharge/whereandwhen/”, Retrieved on 21st, March, 2013

The LCC fee is charged from Monday to Friday each week, 07:00 a.m. to 18:00 p.m. each day upon motorists operating in CCZ, and “no charge on weekends, public holidays, between Christmas Day and New Year’s Day inclusive, or between 18:00 p.m. to 07:00 a.m.” [1] The LCC is £5 per day per motorist when this policy was introduced, and it increases to £10 per day now. There are exemptions – “vehicles such as emergency service vehicles and Black cabs licensed with Taxi and Private Hire (TPH) can drive in the zone free”. [2] The CCZ covers about 136,000 residents in London. There are a temporarily expansion of CCZ from February 2007 to January 2011 to include the western London – called western extension. But it was cancelled after a large public consultation in 2008, which showed that about 67% of London residents and 86% of business disliked this extension.

Discussion

(I) Implementation evaluation. According to the Transport for London official website, there is “a 6% increasement in bus passengers during the charging hours” and “all net revenue raised by this charge (£148million in financial year 2009/2010) has to be invested in improving transport in London, by law.” [3].

It seems that the government evaluate this policy success in the aspect of increasing traffic flows. However, since the unclear statement here (they don’t point out the increasement happens in busy period or leisure period). Thus, using the “raising usage of public transportation” as an evidence, I could not conclude that the congestion reduce. An important indicator of the traffic flows is the average traffic speeds. If the government could show that the average vehicle speeds in CCZ during busy hours increase by 6%, then I could conclude that this policy do reduce the traffic. Leape (2006) summaries that the number of private cars, vans and trucks coming into CCZ dropped by 27% between 2002 and 2003. To the best I could do, there is no persuasive paper for the latest data.

Since the UK keeps a nice developing speed in the previous years, and the statement of “increases in congestions” on TFL official website, the best guess I could made on the policy implementation after 2011 is that the policy succeed at the early years after it was introduced, then the traffic flows level has dropped back to pre-charging level due to the increasing of income, and reducing of the road capacity.

(II) Tax revenue. According to the government’s statement of the policy revenue, the net tax revenue would be used to increase the transport system in London. I could not find the financial year book talking about how they invest the net revenue and the outcomes of this investment. And due to the financial crisis in EU area, the indicators of the transportation systems would be affected by other economic factors. Leape(2006) points out that there is a shortfalls in the tax revenue because of unexpected operation cost, and some 80% have been invested on bust network improvements in 2003-2004 and further 11% expense on road safety; and the annual social total cost in 2005 ( when LCC is £5) is £163 million while the annual social total benefit is £230 million. This findings implies that the policy shows an improvement in both private and social sections. And the Wikipedia of LCC shows that the net revenue increased continuously from 2004 /05 to 2006/07. However, the financial crisis and the lack of latest data could not support this conclusion after 2011. To my best knowledge, I could only say that if they continue the investment and the LCC fee ( £10 per day now) is still reasonable – neither too high nor too low, the social and private would both benefit from this tax revenue via the improvement of public transportation.

(III) Distributional effects. In part, I would focus on the air quality, parking issue, traffic accident rate and traffic speeds instead of income of poors and riches. I would separate the London as CCZ and Non-CCZ areas, the difference is that the Non-CCZ area does not have LCC ( include the western area since the extension has been opposed.)

As the policy review at the beginning of this blog, the CCZ locates in the central of London – the busy area and central of a capital city. The LCC would help to control the traffic congestion level within the CCZ via raising the individual opportunity cost of entering the CCZ. Theoretically speaking, the raising individual opportunity cost could make the total private cost convergence to the total social cost. Using the typical Gornor fishery model, regarding the fishery capacity as the road capacity, the effort as the entering vehicle, we could obtain an optimal allocation consisted of the entering vehicle level and the capacity level. In this optimal allocation, the CCZ would have a better statue compared with no-policy.

However, in Non-CCZ areas, series of problems would appear. People who value the time higher than LCC and parking fee in CCZ would continue to drive into CCZ in busy hours, and others who do not willing to pay the LCC and have a lower value of the time would choose public transportations. The “middle” part, covered most of middle-income level family, they could not support LCC and expensive parking fee in the central London, but value the time, would choose to drive to the boundary of CCZ and switch to public transportation system. With these actions, the burden of public system inside CCZ would higher, the parking fee around the boundary of CCZ would increase, and the potential traffic congestion in the boundary area would appear. If the government could not solve these problems efficiently, the new traffic congestion around the boundary area would raise the traffic congestion level inside the CCZ. And the CCZ would enlarge continuously with the same problem.

Talking to the traffic accident, the LCC higher the opportunity cost of cars, people would switch to either public transportation options or other vehicles that are not charged. Daniel J. Graham et,al. (2012) use the difference-in-difference model integrated with Poission and Negative Binomial regression model to test the regional effects of LCC, and concludes that this policy reduces the total car accidents but increases the two wheels vehicles accidents

In my opinion, the optional strategy is the area-based LCC. TFL could set different level of LCC in different CCZ. Individuals would select their affordable LCC. The burden of public system could be spread out as well. The supporting theorems of my suggestion are partial equilibriums and incentive mechanism. It looks like a government sponsored firm uses the price discrimination to achieve a better allocation.

By

Catherine Guo

(The author shows grateful to suggestions of policy selection from best friend Rayla Liu, 2nd year Ph.d student of UVA)

Reference:

[1]Transport for London (TFL), http://www.tfl.gov.uk/tfl/roadusers/congestioncharge/whereandwhen/, Retrieved on 22nd March, 2013.

[2]Transport for London (TFL), http://www.tfl.gov.uk/roadusers/congestioncharging/6713.aspx, Retrieved on 22nd March, 2013.

[3] Trasnport for London (TFL), http://www.tfl.gov.uk/roadusers/congestioncharging/6723.aspx , Retrieved on 22nd March, 2013

[4] London Congestion Charge (LCC), http://en.wikipedia.org/wiki/London_congestion_charge#Effects , Retrieved on 22nd March, 2013

[5] Leape Jonathan, The London congestion Charge, Journal of Economic Perspectives, Volume 20, No.4, Fall 2006, pp. 157-176

[6] Daniel J. Graham, Haojie Li, Arnab Majumdar, The Effects of Congestion Charging on Road Traffic Cusualities: Analysis Using Difference-in-difference Estimation, Accident Analysis & Prevention, Volume 49, Nov. 2012, pp.366-377

{kind=link}