France Water Effluent Tax

It is been historically well known that the US prefers tradable permits, especially the freely allocated, grandfathered permits while the EU prefers taxation. This difference could be seen as a reflection of a stronger belief in individual private rights and specifically the “prior appropriation” doctrine (the right of the first user) in the US. On the other hand, Europe is rather in favor of the benign and paternalistic state, working with “societal” interests in mind. Therefore, I would like to write about a EU pollution tax, particularly the France water effluent tax.

Basically, France has no considerable problem with quantity aspect of water resources due to favorable climatic conditions. Hence, France focused on the quality aspect of water management policy, which is the reduction of water pollution.

The players and coverage of the France water effluent tax system

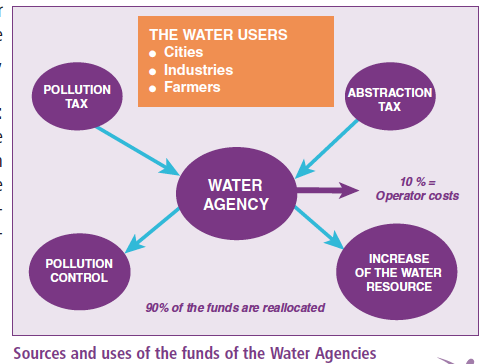

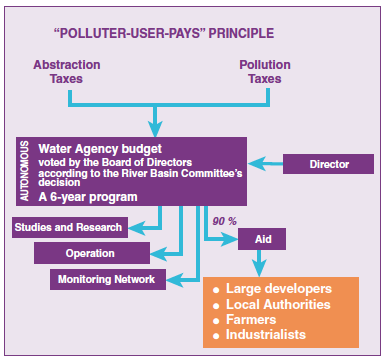

- The framework for water charges was created in 1964 and was managed by six basin-wide institutions, the Water Agencies that are jointly controlled by the State and municipalities. The water charges system covers the whole of France.

- Charges may be levied on any agency (public or private groups) or any individual if they:

-Lead to the deterioration of water quality:

-Extract water for use from natural sources; or

-Change a river basin’s marine environment.

- The effluent tax is proportionally imposed on the polluters by the quantity of pollution they discharge.

- The charge includes a wide variety of pollutants (suspended solids, biological oxygen demand (BOD), chemical oxygen demand (COD), toxic substances, phosphorus, nitrates and several heavy metals).

The use of revenue from tax

The effluent charges collected are earmarked for promoting pollution abatement activities (to build waste treatment plants). In other words, a compensation system, known as the subsidy for wastewater treatment, was used to offset the water pollution charge for those people or bodies who treat water before discharging it into rivers and lakes. Revenues are thus totally redistributed to those engaging in pollution abatement (industrialist or municipalities responsible for treating household effluents), according to investment costs, and not pollution performance.

The ‘last time’ Problem

Since the creation of Water agencies in 1964, there has been an incessant disagreement over charge rates between the State and the municipalities. The political economy is central to the evaluation of the effluent tax rate. To be precise, the charge rate could be perceived as the outcome of a three players’ game involving the Ministry of Environment (maximizing polluter’s compliance with water regulations), the Ministry of Finance (minimizing Agencies’ budget), and the municipalities (maximizing political support). As a result, the rate of the effluent tax maybe too low to stimulate a noticeable incentive effect on water consumers and polluters.

The gist of the story is that the charges and subsidies are effective in promoting regulatory compliance among the individuals and groups but is not effective enough to induce the polluters to go beyond regulatory requirements (the French water system is constrained to a role of enforcement of public regulation due to the hybrid nature of the Water Agencies).

The current France Water System

- There are two categories of tax: the pollution tax (aims at preserving water quality) on the emission of pollutants and water abstraction tax (to promote water saving).

- 7 types of taxes:

-Water pollution tax

-Tax for modernization of wastewater drainage systems

-Tax on non-point agricultural production (farmers)

-Water abstraction tax

-Tax for water storage in low flow periods

-Tax on obstacle on rivers

-Tax for the protection of aquatic environment

- Tax calculation is based on a regular follow up on discharges.

-For households, the water tax is calculated for each municipality according to permanent and seasonal populations and levied through drinking water bill paid by consumer in accordance to the consumed volume measured by the meter.

-For agricultural uses, a new tax has been implemented in 2008 by all distributors of phytosanitary products according to the quantity of dangerous/ toxic substances contained in the marketed products.

- The tax revenue is not tax neutral, as the population is not being paid back the tax. As mentioned before, the tax is earmarked for investments mad by municipalities, industrialists, farmers and other users to preserve the water resource and to improve the performances of the treatment plants. One thing to note here is that a proportion of the investment is subsidized relative to the size of the investment and not the overall pollution performance. This may be a little undesirable as there may be no evaluation (cost benefit analysis in terms of net present value) of the projects before giving out the subsidies to the industrialists.

In conclusion, France’s water allocation and pollution control is a “public utility” model and rely on centralized administrative discretion and less on the preference and initiatives of private individuals. Water charges are set without regard for scarcity values based on bids and offers by consumers. In addition, there may be a lack of congruence between regulation and economic incentives (taxes) rooted in the competition between the two institutions. The water tax is definitely effective at the regulation level, however, it may not be high enough to promote initiatives by the polluters to take a step further to reduce water pollution.

References:

http://www.rff.org/documents/RFF-DP-01-58.pdf

http://www.iisd.org/greenbud/france.htm

http://www.fao.org/docrep/003/t0800e/t0800e0c.htm

http://www.oieau.org/IMG/pdf/IOWater-WaterManagementFrance.pdf

http://www.cerna.ensmp.fr/Documents/MG-Sub-EuropeanJalLawEco.pdf

Comments