By now most people have heard of cryptocurrencies like bitcoin, but where does this currency come from? Much like gold, there is a fixed amount of bitcoin, 21 million bitcoins to be exact. These bitcoins can be ‘mined’ using computers running a special algorithm. In the past miners would use old computer hardware, specifically GPUs (Graphics Processing Units) which are typically used for computer gaming. This meant it was very easy for someone with a gaming computer to make some extra money by letting their computer run the mining algorithm while they were not using their computer.

Gaming GPU: Wikipedia Commons

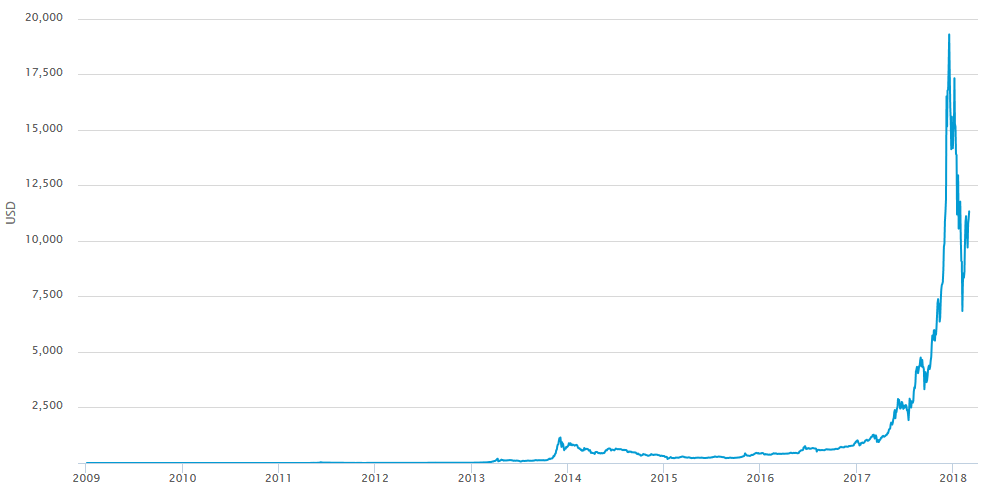

As cryptocurrencies such as bitcoin become more mainstream, its value skyrocketed. This drove more people to become miners. More miners and newer, more powerful GPUs in computers lead to many bitcoins being found. So far, this sounds great, so should you go out and buy a GPU and become a miner?

Bitcoin Prices: Wikipedia Commons

Here’s the catch; as more bitcoins are found, it quickly becomes much more difficult to mine. This is because of the way bitcoin is setup. Because there is a fixed amount, it is very easy to mine the first bitcoins, but as more are found, the remaining bitcoins become much more rare. This rarity and huge popularity causes the value of bitcoin to rapidly inflate, causing more people to become miners.

One might ask, is mining profitable? The answer is more complicated then you might expect. Back when miners were just using old computers to mine, the only cost they had to worry about was electricity, and yes it was very profitable. Nowadays you need much more powerful hardware and multiple GPUs to mine. Although GPUs have become more efficient, multiple GPUs will still consume a lot more electricity than a single older one. Not only that, GPU pricing has also sky-rocketed, much to the dismay of computer gamers.

So with all these variables taken into consideration, let’s see what it would take to become a miner. First you would need an extremely powerful computer with as many GPUs as possible. For our example lets say we use 8 high-end GPUs. This system would cost around $18,000 and would make around $11 a day in profit (assuming your electricity rates are relatively low in your area). This means it would take over 4 years to just break even and that is assuming the cryptocurrency market remains stable, which it is notorious for being very unpredictable. So no it is not profitable to be a cryptocurrency miner using regular computer hardware, unless you already have the GPUs. Nowadays, you are better off using dedicated mining machines or just trading cryptocurrencies on the stock market, if you are trying to make some extra money.

Dedicated mining machine: Wikipedia Commons