Hi Team Undefined,

I have revised my definition of ‘Accrual Accounting’ to incorporate the feedback received from Elton Kok. Please see the attached Word Document where I have included tracked changes for your convenience.

301 Richard Chen Definition Revised

Thank you,

Richard

Peer Review: https://blogs.ubc.ca/engl301-99a-2020wa/2020/10/04/assignment-13-peer-review-of-definition-of-a-accrual-accounting/

Original Definition: https://blogs.ubc.ca/engl301-99a-2020wa/2020/09/30/assignment-13-definition-of-accrual-accounting/

__________________________________

Introduction

The objective of this week’s assignment is to define a technical term in a way an audience of non-technical readers find easily comprehensible. Being able to identify the audience and their level of understanding, as well as plausible situations the audience would encounter the term is crucial.

The definition will consist of a parenthetical, sentence, and expanded definition. As my background is in the accounting field, the term I have chosen is accounting related.

Term:

Accrual accounting

Situation:

A new small business owner is asking a Chartered Professional Accountant what ‘accrual accounting’ is, and why it is relevant to his/her business.

Parenthetical Definition:

Most businesses use accrual accounting (recording transactions when the related work has been performed) when reporting taxes or presenting financial statements.

Sentence Definition:

Accrual accounting is a method of recording transactions at the time when revenue is earned, or expenses incurred rather than when cash exchanges hands. Earning or incurring is deemed to have happened when the related activity has been completed.

Expanded Definition:

Accrual accounting is the most common and accepted form of accounting used by large and small businesses around the world.

In this method of accounting, transactions are recorded when the related activity has occurred. An ‘accrual’ is the recording of revenue or expenses that have not yet lead to the exchange of cash (Kenton, 2020). Under the most common accounting standards, revenue is recorded when the following three conditions are met (Deloitte, 2020):

- The business has performed its obligation as required to the customer

- The amount of revenue can be measured reliably

- It is probable that payment can be collected

Note that under these conditions, payment does not need to have exchanged hands for the revenue to be recognized. Instead, payment only needs to be measurable, and it is reasonably expected that payment will be collected.

Similarly, expenses should be recorded on a basis of when they are incurred to generate revenue. Generally, all expenses are incurred by a business to generate revenue directly or indirectly. It is an accounting principle to match the expenses related to a revenue transaction within the same fiscal period (CFI, 2019).

The alternative to accrual accounting is cash-based accounting. Many people will already be familiar with this or have some intuition regarding it, as they may be using it to manage personal finances. In this method of accounting, transactions are recorded only when payment is rendered. Cash-based accounting is much simpler, however it can result in an inaccurate depiction of one’s finances. The inaccuracy mainly relates to the time difference between when the revenue is said to have been earned or expense incurred as dictated by the criteria above, and when payment occurs which can be several weeks or months. An example of this inaccuracy is given below. Cash accounting’s inherent inaccuracy is what gave rise to the adoption of accrual accounting.

Cash based accounting is typically reserved for farmers, self-employed commission sales agents, and other niche businesses (CRA, 2020).

The concept of accruals has existed since the seventeenth century but was not popularized until the nineteenth century (Ovunda, 2015, p. 135-136). Some of the issues presented by cash accounting that prompted the moved to accrual accounting was that it did not accurately reflect the financial situation of company. For instance, imagine a company uses the cash method of accounting and has received goods & services in a fiscal year. However, under the payment terms the company does not pay need to pay for these goods & services until the next fiscal year. Under the cash method, the transaction would not be recorded until the payment has been made in the next year. Under the accrual method, the transaction would be recorded in the current fiscal year. The accrual method is argued to depict a more accurate image of the company’s financial situation, as it owes that money to another entity and in a sense has already been ‘spent’ (Morah, 2020).

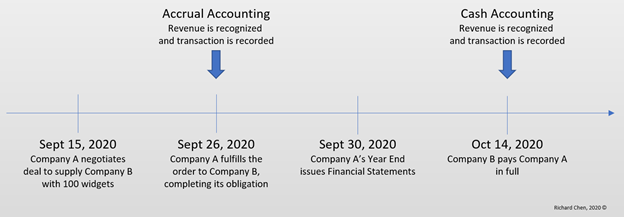

To illustrate an example, refer to Figure 1 below, and suppose Company A enters a deal with Company B to supply 100 widgets. Under accrual accounting, Company A would recognize revenue on Sept 26th as all three conditions have been satisfied. Under cash accounting, revenue would not be recognized until Company B pays Company A. Notice that Company A’s financial statements are issued on Sept 30th. Under cash accounting, the revenue from this deal would not have been recognized even though Company A had performed its obligation. Therefore, accrual accounting provides a more accurate depiction of a company’s financial status, and is less likely to mislead stakeholders reading the financial statements.

Figure 1. Accrual accounting example

References

CFI. (2019, October 02). What is the Matching Principle? Retrieved October 01, 2020, from https://corporatefinanceinstitute.com/resources/knowledge/accounting/matching-principle

CRA. (2020, April 21). Government of Canada. Retrieved October 01, 2020, from https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income/business-income-tax-reporting/accounting-your-earnings.html

Deloitte. (2020, July). IAS 18 — Revenue. Retrieved October 01, 2020, from https://www.iasplus.com/en/standards/ias/ias18

Kenton, W. (2020, September 16). What Is Accrual Accounting and Who Uses It? Retrieved October 01, 2020, from https://www.investopedia.com/terms/a/accrualaccounting.asp

Morah, C. (2020, March 7). Accrual Accounting vs. Cash Basis Accounting: What’s the Difference? Retrieved October 01, 2020, from https://www.investopedia.com/ask/answers/09/accrual-accounting.asp

Ovunda, A. S. (2015). Luca Pacioli’s Double-Entry System of Accounting: A Critique. Retrieved September 30, 2020, from https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.954.6155&rep=rep1&type=pdf

Leave a Reply