Background:

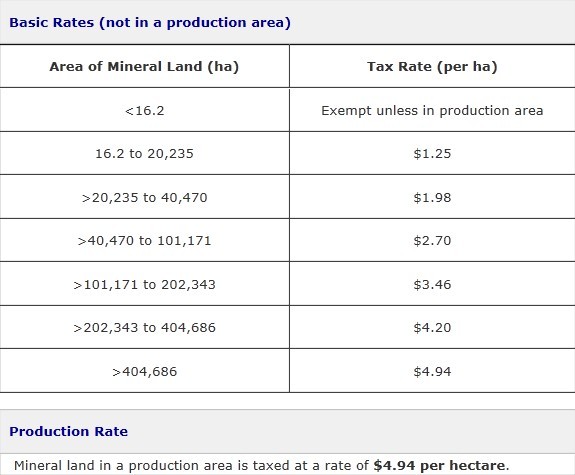

The BC Mineral Land Tax Act is tax levied on owners of freehold mineral rights. Before 1950, the Crown sometimes granted freehold ownership of minerals with the ownership of the surface land, or by grants of ownership of the minerals only. Such areas comprise a small portion of the province. For the rest of the province, the government rents or leases rights to minerals under tenure legislation such as the Mineral Tenure Act, the Coal Act or the Petroleum and Natural Gas Act. The tax was proposed by the Left because they believed the resource in BC belongs to all British Columbians. Mining comanies have to pay taxes to return the province. High mineral tax was strongly opposed by both mining companies and the Right. They claimed that high resource tax will reduce competitiveness and this will decrease employment rate. The Mineral Land Tax is assessed annually at $1.25 to $4.94 per hectare, depending on the amount of land to which the owner has freehold mineral rights and whether minerals are being produced from the land.

Goal:

The Mineral Land Tax Act is tax levied on the small number of land owners in the province granted mineral rights under land before 1950. The purpose of Mineral Land Tax is to provide a return to the province from commercial use and depletion of the province’s coal and mineral resources.

Coverage:

Mineral Land Tax rates are based on the size of the mineral land and whether or not the land is in production. There are only two types of exemptions:

1. Charitable Exemptions:

Registered charitable organizations are exempt from the payment of Mineral Land Tax. Please contact us with your charitable registration number to claim this exemption.

2. Agricultural Exemptions

The Mineral Land Tax Act provides for a classification of “agricultural mineral land”, where the land is used primarily for agricultural purposes. Land classified as agricultural mineral land must be assessed under the Act, but no tax is payable. Please see the Application for the Classification of Agricultural Mineral Land for more information.

Tax Rate and Tax Revenue:

As we can see from the table above, Mineral Land Tax rates are based on the size of the mineral land and whether or not the land is in production. Not later than July 2 in every year, owners of mineral lands must pay the tax. If Mineral Land Tax remains unpaid for two consecutive years, the mineral rights become subject to forfeiture, which means they can be taken away by the government. A person can choose to surrender all or part of an interest in mineral land to the government at any time.

Refunds are available in order to reward mining exploration. Normally, 20% of exploration expenses fund by the government and the revenue raised from Mineral Land Tax is strictly used for environmental expenditures. The corporation or partnership must incur qualified mining exploration expenses before January 1, 2017 for determining the existence, location, extent or quality of a mineral resource in B.C.

Cost-Effectiveness and Distributional Impacts:

About the cost-effectiveness of the policy, I believe this policy is necessary. First of all, as the Mineral Land Tax is implemented, both the consumers and producers are hurt and deadweight loss was formed. However, as the government rewards mining exploration by refunding 20% of the exploration expenses, the deadweight loss decreases. Second, except for Mineral Land Tax, there is also a Mineral Tax. Mineral Tax is levied on operators of mines (including placer mines) and quarries. As we can see, both taxes are imposed on mining companies and they are somehow overlapping. The goal of Mineral Land Tax is not increasing revenue, but saving resource, protecting environment and reducing pollution. The Mineral Land Tax alone is not high, but together with Mineral Tax, mining companies have to be careful when exploiting resource since they have to pay for both the land and their production. It is obvious that these two policies can save resource and reduce waste. I believe the total policy cost is acceptable because saving resource and reducing waste are more important. With the policy, a new optimal exploiting level is formed and the market will move to the optimal level by itself.

Is Mineral Land Tax an important tax for mining companies in BC? I’m afraid it is not. For example, in 2011, the total Mineral Land Tax in BC is only $601,000 while Mineral Tax is $363,911,000. In 2012, the total Mineral Land Tax in BC is $594,000 while Mineral Tax is $357,706,000. Mineral Land Tax is only considered as land rental cost. It is not a major expense. So, unlike Mineral Tax, it won’t affect mining companies decisions. However, I think it will be a good idea to eliminate Mineral Land Tax to reduce administritive costs and reduce burden to the mineral extraction companies. I believe a tax on mineral company is necessary and these two taxes can merge into a new mineral tax.

As the government rewards mining exploration by refunding 20% of the exploration expenses, how will the policy affect people? Well, it is obvious that producers can reduce some of the cost and consumers can also pay less. However, they still need to pay more because of the tax. After the tax, the price will go up and demand will decrease. Both producers and consumers will pay for the tax. The amount of paying based on the slope of supply and demand curve. However, as the government refund the tax, both individuals and business can get some benefit.

How can mineral tax affect the market? I can give an example. In 2011, Australia announced that a 30% Mineral Tax was imposed for mining companies with annual profit of $75 million. This is a compromise because the government had planned to impose a 40% Mineral Tax. More Mineral Tax is a new international trend. However, it will hurt both the producers and consumers. Chinese buyers decided to buy more ore from Africa instead of Australia. Of course, the ore price in Africa will also increase because of the increasing demand. Australian mining companies claim that the tax imposed by the government makes them earn less and the policy will destroy Australian mining industry.

Conclusion:

So, in total, the mineral tax policy in BC can hurt business and consumers at the same time, but it is friendly to environment. I do think a refundable mineral tax is necessary since it can save resource and reduce the deadweight loss at the same time. However, since Mineral Land Tax is not important enough to affect decisions of mining campanies, my suggestion is that we can cancel Mineral Land Tax and impose a little bit more on Mineral Tax. It is more cost-effective and time-saving effort.

Reference:

- http://www.sbr.gov.bc.ca/business/Natural_Resources/Mineral_Land_Tax/mineral_land_tax.htm

- http://www.sbr.gov.bc.ca/business/Natural_Resources/Mineral_Tax/mineral_tax.htm

- http://www.sbr.gov.bc.ca/business/Natural_Resources/Mineral_Tax/minrev_collected.pdf

- http://www.bbc.co.uk/news/business-17441170

- http://www.sbr.gov.bc.ca/business/Natural_Resources/Mineral_Land_Tax/MLT_Act.pdf

Hi Peter,

Mineral and land tax is indeed an intriguing topic. Glad you’ve chosen this one! I agree on you that by eliminating one of the two taxes could help reduce administrative costs and reduce burden to the mineral extraction companies. In my understanding, taxes do impose a price distortion, thereby, generatng a dead weight loss on society. However, we are never certain the welfare effects, depending on the tax rate, and the nature of market price elasticities. Would you think that if instead the government issue a quota (permit) at market value to the extraction companies, it’d generate far more economic benefits both to firms and government?

Vicki

Thanks Vicki! Using quota is a good idea! People can buy quota from other companies too~

Hi peter 🙂

Before I read your blog, I definitely had no idea that BC has a mineral tax.

Thanks for sharing interesting information!

Thanks Cindy. Mineral Land Tax is a some tax~ You can consider it as a land renting cost.

Good blog Peter! It is amazing that you could find so much relevant data on the topic. You do mention some distributional impacts and how the tax is levied. However, I found inadequate information on the political origins of the policy. It would be nice to know which party (Liberal or Conservatives or NDP) and under which premier enacted this regulation. But, all in all, this is a good effort and a unique topic of focus. Looking forward to reading more of your blogs in future. Ahmed

Thanks for your advices Ahmed~ I found it is always difficult to find the origins of policies. Especially when the policy was introduced many years ago.

Very interesting to do something that’s so local, Peter! You believe it would be more cost and time efficient to remove one of the taxes, specifically the Mineral Land Tax as it doesn’t affect companies’ decisions significantly enough, but would that have any effects on…let’s say entry into the industry? By removing this tax, would it have an impact on barrier to entry and more attractive now?

Thanks Lisa. I think the land tax won’t affect so much since it is too “cheap” for mining companies to consider. Mineral tax can affect a lot since it is more “expensive”~