GOAL:

To properly price the disposal of waste by landfill: the cost of landfill in the UK was low compared to other European countries, and failed to internalize the social cost of environmental impacts

To encourage efforts to minimize the waste produced, and the use of non landfill waste management options, such as re-using, recycling, and composting.

Background

In 1996, the Conservative government of the United Kingdom published a strategy to develop plans for sustainable waste management, and promised to achieve a 25% recycling rate for household waste. The UK Landfill Tax was a part of this strategy; it was brought into existence by the Finance Act 1996 and officially began on October 1st, 1996. The UK Landfill Tax was hailed by the UK government as its first environmental tax.

What is Landfill and Landfill Tax?

Landfills are solid waste disposal sites, where waste is deposited, compacted, and periodically covered over a layer of soil. There are two types of waste – active and inactive (inert). Inert is classified under inactive waste, which includes a broader variety of classifications of waste. Inactive waste covers most materials used in a building fabric, and most forms of concrete, glass, and soil, etc. Active waste covers all other forms of wastes, such as wood, and plastics.

Landfill Tax is an environmental weight based tax on the waste disposal to landfill paid by the local companies, authorities or organizations. All landfill site operators with license or permit for landfill sites are liable to pay the tax. However, they will pass the tax onto the local businesses by charging a cost on top of normal landfill fees.

Tax Coverage

Unless it is specifically exempted, landfill tax applies to all material disposed of as waste.

Exemption

Waste removed from inland waterways and harbours via dredging and disposed of to landfill is exempted from landfill tax. Any naturally occurring substances which result from extraction of sand, gravel or other materials from the seabed as part of commercial operations, qualify for the exemption. Since 2007, the exemption has been extended to apply to waste disposals where additives that contain dehydrating properties are added to ensure it’s not in liquid state. Additionally, waste produced from mining and quarrying operations is also excluded. Burials of dead pets are not taxable, even though pet cemeteries are allowed to be treated as landfill sites under the environmental law.

Landfill Tax Rate

In general, the environmental taxation rate is usually established in one of two ways. The rate is set to:

- charge for the social cost of the negative externality per unit of taxation

- achieve particular targets such as to reduction in landfill demand by increasing the landfill cost

It is common to have the tax escalation over time until the desired objectives are achieved.

UK Landfill Tax Rate

In the UK, an escalator approach to taxation has been adapted since the landfill tax analysts suggested that the impact of the externality based tax was small. The alternative method was recommended to achieve environmental targets in 1998.

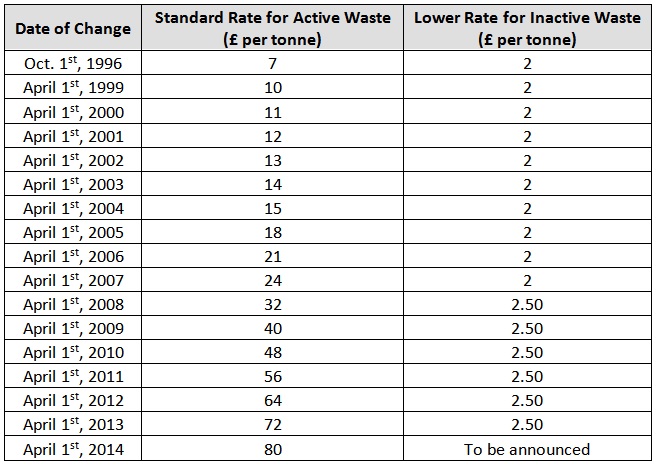

The amount of tax levied is calculated according to the weight of the waste disposed of, at two different rates depending on whether the material is active or inactive waste. The lower rate applies to the inactive waste, which pollutes less waste, and the standard higher rate applies to all other taxable active waste.

When both standard and lower rated materials are contained in the waste, the rate used is determined by the form of material that dominates the waste. For example, an incidental amount of standard rated waste is disregarded, if the mixture is composed mainly of lower rated materials, and the whole load is taxed at the lower rate. Also, all materials are taxed only once. For instance, if 80% of the materials are new, and 20% of the waste has been taxed before, tax is only due on the 80% of the new waste.

The government Emergency Budget 2010 announced that the standard landfill tax rate will increase by £8.00/tonne annually from April 2011 until at least 2014. There will be a price floor which prevents the rate to drop below £80.00/tonne from 2014/2015 to 2019/2020.

Appropriate?

Assuming the reduction in waste production and the landfill prevention are tightly associated, the marginal social benefits of avoided landfill are undoubtedly very high. Extended externalities analyses have proven rational for a much higher taxation rate.

Tax Revenue

The revenue raised from the landfill tax is strictly used for environmental related expenditures, and reduce other taxes. The tax revenue is hypothecated back to the tax payer through reduction in the national insurance paid by businesses. The Landfill Tax Credit Scheme (LTCS) allows the landfill operators to receive tax rebates by making contributions in projects (i.e. maintenance or improvement of a public park in the area near a landfill site) approved by Environmental Body (EB).

What is Landfill Tax Credit Scheme (LTCS) and How does it work?

The LTCS, introduced as a part of the Landfill Tax regulation, was designed to distribute funds generated from the UK Landfill Tax. It was used to mitigate the effect of the landfill tax in local communities, encourage partnerships between landfill operators, local communities, and the public sectors and create environmental benefits and jobs through projects that improve the lives conditions near landfill sites.

With the LTCS in place, land operators with contribution record are allowed to contribute up to 20% of their annual landfill tax liability to EB, who disperse the money through project funding. The land operators are then allowed to reclaim 90% of these funds; in other words, the LTCS hypothecates 20% of landfill tax revenue.

Effectiveness of the Policy

The landfill tax has a relatively low impact on the disposal and production of waste in the UK. There is an apparent increasing in recycling and reuse, but the gradual increase is offset by the rapid growth in municipal waste. There are three main reasons explaining the ineffectiveness of the tax:

- The tax on municipal waste is insignificant, that the waste producers have no financial incentive to recycle,

- The growing transport cost is an additional cost to the overall land-filling waste,

- Alternative disposal options are taking large quantities of waste.

In addition, many products seem to have reached a plateau caused by market constraints.

As a major stakeholder, and responsible for 40% of the tax raised, the local authorities had little voice on the operation of the tax; majority of them felt that they had no choice but to pay the tax. Furthermore, the tax has been ineffective in changing the behavior of most potential producers of polluting waste: domestic households, and small and medium enterprises. Integrated with the other taxes, the landfill tax is charged at a flat rate for the households, and gives them no incentive to reduce waste production. Concerning businesses, the tax is too small of a cost to enforce change in behavior that is directly linked to waste production. Moreover, the landfill operators have little interest in funding recycling, as they do not directly benefit from the LTCS.

While the LTCS is currently the main environmental benefit resulting from the tax, the EBs are not dominating it with projects that promote sustainable waste management and achieve the overall objective of the landfill tax. To conclude, the landfill tax is at present ineffective, and it has made limited contribution to environmental sustainability.

Conclusion

Weighting the cost and effectiveness of the UK landfill tax, I personally do not think the tax is revenue neutral. The overall input is clearly outweighing the output, and the marginal damage created by the waste is not in equilibrium with the benefit generated from the tax. While the LTCS did generate some environmental benefit, the change in behavior of the waste producers and reduction in the waste produced generated directly from the tax have not been significant. Majority of the landfill tax was blended in with the other taxes, and left little financial incentive for the domestic and commercial waste producers to reduce their waste production. While tax payers feel the additional burden from the landfill tax, the money collected is not put into best use, and the potential effect of the tax are not maximized. In my opinion, the tax needs to be reallocated, and redesigned, and a higher landfill tax has to be charged to increase the effectiveness of the tax, as well as the awareness by taxpayers.

In conclusion, by simply raising the landfill cost via tax, and expecting the producers to turn to other waste management methods without providing additional financial support is clearly not enough to achieve sustainable waste management goals. In the case of the UK landfill tax, the relevant parties have not done what they proposed to do, and the goal of the tax has not been met at present.

Reference

http://ec.europa.eu/environment/enveco/taxation/pdf/ch15_uk_landfill.pdf

http://economicinstruments.com/index.php/component/zine/article/223

http://www.economicinstruments.com/index.php/solid-waste/charges-and-taxes-/article/222-

http://www.politics.co.uk/reference/landfill-tax

http://www.tandfonline.com/doi/pdf/10.1111/1467-9302.00224

12 replies on “The United Kingdom Landfill Tax”

Hi Vicky,

I also have been following the European landfill taxation policies on my part. Consider the inffectiveness of the UK landfill tax policy, should the government devise subsidies or tax rebates to reward industries for diverting waste from landfilling? Alternatively, would it be possible that landfill waste could become exportable waste for incineration to ISSÉANE, the largest incinerator, in France.

Hope you enjoy the rest of your weekend!

Vicki

Hi, Vicki,

To address your question on the exportation of the waste, the UK bans the import and export of waste for disposal, to support “the UNEP Basel Convention on the Control of Transboundary Movements of Hazardous Wastes and their Disposal”, which is aimed to protect human health and environment against the adverse effect resulting from the disposal of hazardous and other wastes. This leads to a completely different topic/issue. In general, there is no import into or export from the UK, though waste can be traded between the UK and other countries to help reserve natural resources and economically benefit the UK.

Right, presumably the countries involved are trying to minimize disposal of hazardous waste, and minimize the toxicity of waste generation the so-called “Toxic Colonialism” among many LDCs.

I’ve read from the Tyser’s development article that the UK is trying to reduce desamenities from landfill. The country is facing scarcity in land.. essentially to tackle this issue, nowadays, it is not uncommon that many sites are situated in prominent urban locations, ie: The Shaw Forest Park with green oasis surrounded by urban housing and industrial centre. The Park was formerly a landfill site.It is now restored as a public open space for sustainable development.

Once again, thanks for the enlightening blog post. Look forward to unravelling more critical issues for further discussions! If you could spare sometime, feel free to visit my blog on The Netherlands landfill taxation.

Cheers,

Vicki

wow~I also discuss landfill fee in New Zealand~~~

What’s your opinion about no change on landfill fee? The NZ government dont change the fee and choose a fix rate.

I think they should adjust and increase the rate with the income increase. But it seems unfair since there is no evidence that the supply of wastes increase… I dont know how to discuss with unfair in policy…

Nice blog!

So, based on yours, UK landfill tax is perfectly netural right?

I wrote a blog about Sweden’s neutral NO’X tax. But, I am really wondering the purpose of neutral tax if it would be paid back to people anyway.

Hey Cindy! thanks for commenting. I think the purpose of neutral is to reallocate the money, and reduce distortion and inefficiency. 🙂

Great blog Vicky! Is landfill tax commonly imposed all over the world?

Hey Peter,

I think landfill taxes are nation dependent..so they are not commonly imposed all over the world. 🙂

i like your conclusion. very clear. may i know if the landfill tax covers all parts of UK or just England. UK is definitely one of the best countries that deals with waste.

Hey, CZ,

I do believe that the landfill tax covers all parts of the UK.

I agree with the conclusion you made about the landfill tax policy. According to the policy content,this policy is costly and ineffecient and the tax is revenue neutral. I suggest next time you can use a table or PAM in your conclusion part to it more clear. Cheers!

Thank you for your suggsetion, Jessy! 🙂