FRE525: A blog on Sweden’s NOx Tax Policy

1) The coverage of the policy. Discuss the sector covered and exempted. How does the policy implement over time?

2) Discuss the use of revenue from the tax. Is the tax revenue neutral? That is, it is designed to pay back all its revenue collected back to its population. Is its revenue earmarked towards a particular use? Or is the tax revenue put into general tax receipts?

3) Discuss the appropriateness of the tax rate? Do you believe it is approximately equal to the marginal damage from the pollutant regulated?

Sweden’s NOx Tax policy

What NOx tax is

A NOx tax is a charge on every kilogram of nitrogen oxides (NOx) emitted from large stationary combustion plants.

Background and Policy’s Political Origin

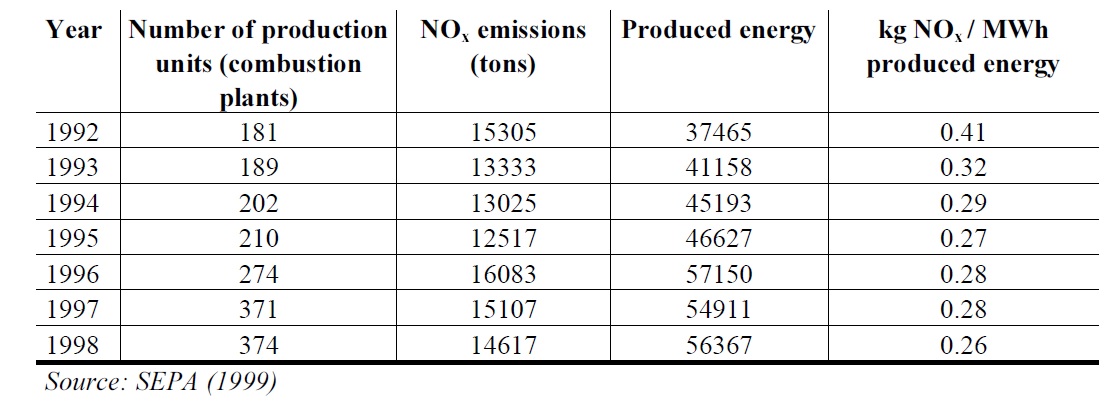

Sweden is one of the countries that has been very vulnerable to acid rain mainly caused by nitrogen oxides (NOx) and sulphur dioxide (SO2). The acidification damages the ecosystem in forests and lakes and human health, and emission of Nox also causes eutrophication in forest soils and on sea beds. As Sweden’s major environmental problem was acidification in the 1980’s, the Swedish Parliament decided to reduce airborne emissions of NOx by 30 per cent by 1995, compared to 1980 levels. With the Swedish Environmental Charges Commission proposal in 1990, a charge of 40 SEK per kg of NOx emitted by combustion plants producing at least 50GWh was introduced on 1 January 1992. The tax system was expanded to include plants producing at least 40 and 25GWh in 1996 and 1997.

Aims

1) Accelerate and stimulate investment in advanced combustion and pollution abatement technologies

2) Allow cost-effective implementation to reduce emissions rapidly by the mid 1990s

How it works

In 1992, combustion plants producing at least 50GWh energy per year were charged by 40 SEK per kg of NOx emitted (or $6.4 per kg). The plants producing at least 40GWh and 25 GWh useful energy per year were also included in 1996 and 1997. The tax rate remains constant. At the beginning of every year, all plants must fill in a form regarding their energy production and NOx emitted for the previous year and send it to Swedish Environmental Protection Agency (SEPA). Most plants measure emissions by using the equipment approved by SEPA. The plants that either have no measuring equipment or whose equipment is temporarily out of order use a standard assessment calculated by1.5times the average emission level. SEPA randomly selects a number of plants each year for inspection. For environmental benefits, the tax revenue except the cost of administration is returned to the participating plants, in proportion to their production of useful energy. The administration cost is approximately 0.3% of total tax revenue.

Coverage

Major sectors covered by Sweden’s NOx tax are the food and beverages industry, wood and wood products industry, paper and paper products industry, metal products – machinery and equipment industry, chemical industry, energy industry and waste combustion industry. Cement and lime industry, coke production, mining industry, refineries, blast-furnaces, glass and isolation material industry, wood board production, and processing of biofuel sectors are exempted due to unfeasibly high costs of metering.

Performance

The policy could successfully lead a huge decrease in nitrogen oxides emissions. From 1992 to 1997, total emissions per unit of useful energy were reduced by 35%. Emission levels between 1992 and 1993 fell by 42% from waste incineration, 23% from energy production plants ,17% from the pulp and paper industry , 13% from the metal industry. With the 1996 and 1997 expansions, which brought 200 new combustion plants into the tax system, total emissions increased. However, the average emission coefficient (kg NOx /MWh produced energy) for the plants actually had been decreasing since 1992.

Tax Revenue

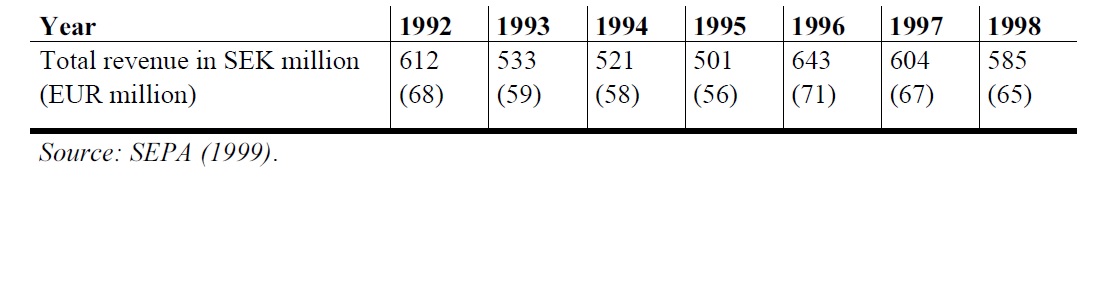

Rather than collecting the tax revenue for the government budget, the tax revenue except the cost of administration is returned to the participating plants, in proportion to their production of useful energy. As the administration cost is approximately 0.2 – 0.3% of total tax revenue, most of the tax revenue are refundable to the plants. Thereby, the tax revenue is neutral. 96% of tax revenue are earmarked for subsidies to abatement investments or for research and development and 4% are used for metering. Any plant paying the NOx tax were eligible to achieve the subsidy. The plants used this subsidy to install emission measuring equipment, to invest in NOx reducing techniques which are combustion method and flue gas treatments (SNCR and SCR).

Tax Rate

Since 1992, the tax rate has remained constant at 40 SEK per kg of nitrogen oxides emitted by combustion plants, in nominal terms. The decision to set the charge at 40 SEK per kg NOX was based on engineering data on expected effectiveness and costs of abatement investments at electricity power stations and district heating plants. The abatement cost was found to range between 3 and 84 SEK per kg reduced NOX. Midpoint of the range is about 43 SEK per kg. A charge of 40 SEK per kg was therefore considered reasonable and appropriate. Unfortunately, there are no empirical studies that show whether the tax rate corresponds to the marginal damage costs. Norway shows that marginal damages from NOx emissions in Norway is about NOK 25/kg. The NOx tax rate in Sweden is SEK 40/kg, or NOK 33/kg. If the marginal damage in Sweden are the same as in Norway, the Swedish NOx tax rate seems to be a little above the marginal damage cost estimated.

Personal Opinion

Based on the information, I can conclude that Sweden’s NOx tax is effective, efficient and fair. Its effectiveness is shown by the reduction in NOx emissions. The annual average emission level was 35% lower in 1992 than in 1990. Since the emissions have been reduced more rapidly than expected, I can say the tax have reduced the emissions efficiently. As the tax system only included larger plants, tax refund prevented unfairness compared to smaller plants exempted by the tax and competiveness to decrease the size of plants. The average abatement cost is 10SKr per kg of NOx emitted. The NOx charge (40Skr per kg) has provided an economic incentive to the plants. The charge is also cost-effective for society. Net social benefit has estimated to be 252 million Skr. The reduction of NOx is usually less successful than SO2 reduction because of technical difficulties. France and Norway failed to reduce NOx significantly. So, I strongly believe that Sweden’s NOx tax policy can be used as a benchmark.

References:

http://books.google.ca/books?id=_rqDi8MA-kEC&pg=PA164&lpg=PA164&dq=sweden+nox+charge+design&source=bl&ots=E65-WZ3keL&sig=yTyDUhqUqhjaVJorgSrDko9V__0&hl=en&sa=X&ei=K3U6UbXQFMPXyAHHxYHgDQ&ved=0CEUQ6AEwBDge#v=onepage&q=sweden%20nox%20charge%20design&f=false

http://ec.europa.eu/environment/enveco/taxation/pdf/ch5nox.pdf

http://www.naturvardsverket.se/Documents/publikationer/620-8245-0.pdf

http://yosemite1.epa.gov/ee/epa/eed.nsf/2602a2edfc22e38a8525766200639df0/f5f2680e0a67338385257746000aff2d!OpenDocument

This is an interesting topic and it is just like carbon tax.

Hi Cindy, what happened in 1996? NOx emmisions and produced energy is relatively high. What happened to this year?

Hi Laura. Thanks for your comment.

To answer your question, I already mentioned it above 🙂

With the 1996 and 1997 expansions, 200 new combustion plants were brought into the tax system. So, it began to measure the level of NOx from additional combustion plants. That’s why the 1996 data had jumped up. I hope this answered to your question.

hi cindy ,

that’s a quiet boring tax. however, i hang in there and did a great job. if there is more measure of the social welfare change and efficiency, it will be perfect. LOL. i can ‘t do it , it’s too difficult!~~XD