Di Wu(Max) | MEL Candidate | Dec 2, 2025

Mentors: Heitor Schiochet, Infinite Grid Capital

Abstract

Traditional BESS valuation models often fail to account for the critical interplay between temperature-dependent degradation, HVAC parasitic loads, and market revenue structures. This project bridges that gap by developing a dedicated investment framework for North American utility-scale batteries.

The model integrates literature-based LFP degradation curves and climate-specific HVAC energy analysis (comparing Edmonton vs. Las Vegas) to simulate realistic lifecycle costs.

Comparative financial modeling reveals that a Pure Arbitrage strategy is commercially unviable (yielding a negative NPV) due to degradation costs. In contrast, a Hybrid Strategy leveraging Operating Reserves achieves a 10.69% IRR and positive NPV. The study confirms that sustainable profitability depends on monetizing the “Speed Premium” of reserves—valuing capacity availability over energy throughput—while implementing rigorous thermal and augmentation planning.

Method

The study integrates a temperature-dependent State of Health (SOH) model with a climate-specific HVAC analysis to simulate realistic asset behavior. Using LFP degradation parameters and historical weather data (Edmonton vs. Las Vegas) , the framework calculates annual capacity loss and determines the timing for augmentation (triggered at 75% SOH). These technical outputs feed into a dynamic financial model that contrasts two distinct revenue strategies: a baseline Arbitrage Only scenario and a Hybrid Strategy incorporating Operating Reserves. Finally, lifecycle cash flows are analyzed to compute NPV and IRR, quantifying the impact of revenue stacking on project viability.

Degradation Analysis

Battery degradation is modeled using a temperature-dependent SOH equation derived from literature-based LFP aging parameters. Theoretical analysis confirms that without thermal control, asset life diverges significantly across 10°C, 25°C, and 40°C scenarios. In practice, active liquid cooling regulates cell temperatures to an optimal 15–35°C band. This strategy effectively neutralizes climate-driven degradation differences, shifting the environmental impact to HVAC parasitic load.

Crucially, the model reveals a 100% variance in HVAC energy costs between cold (Edmonton) and hot (Las Vegas) climates ($0.141 vs $0.067 /kW-year). While this represents a minor fraction of total OPEX compared to augmentation, this sharp contrast proves that location-specific thermal modeling is necessary for precise OPEX forecasting, even if revenue structure remains the dominant financial driver.

| Site | DDH (℃·h) | Energy (kWh/yr,) | Energy cost (CAD/yr) | O&M (HVAC-only) (CAD/kW-yr) |

| Las Vegas – Cooling | 76,824 | 6,970 | $839 (0.1204 CAD/kWh) | 0.067 |

| Edmonton – Heating | 123,019 | 11,161 | $1,763 (0.158 CAD/kWh) | 0.141 |

Results

Model results confirm that revenue structure—specifically the inclusion of ancillary services—is the decisive factor for BESS financial performance.

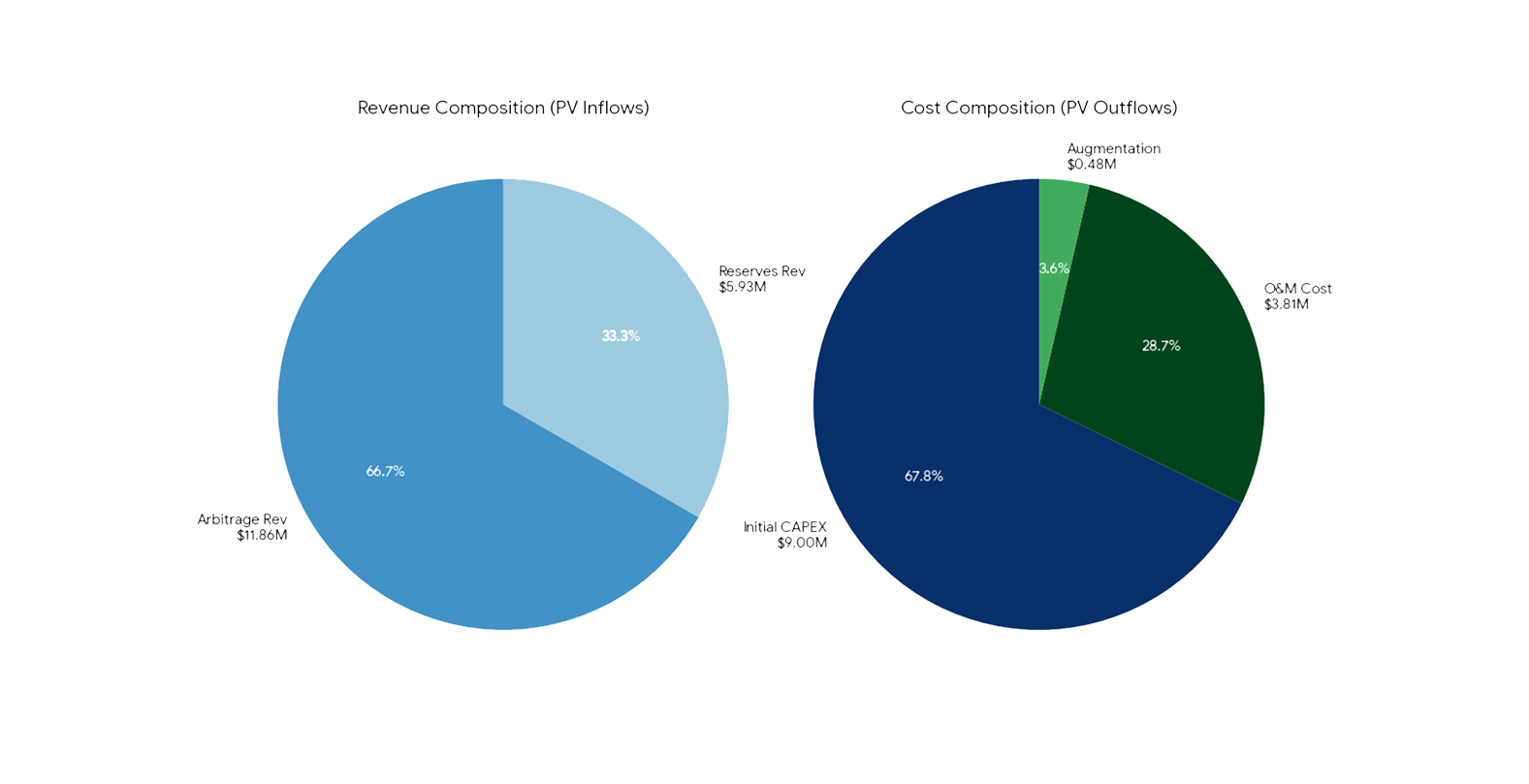

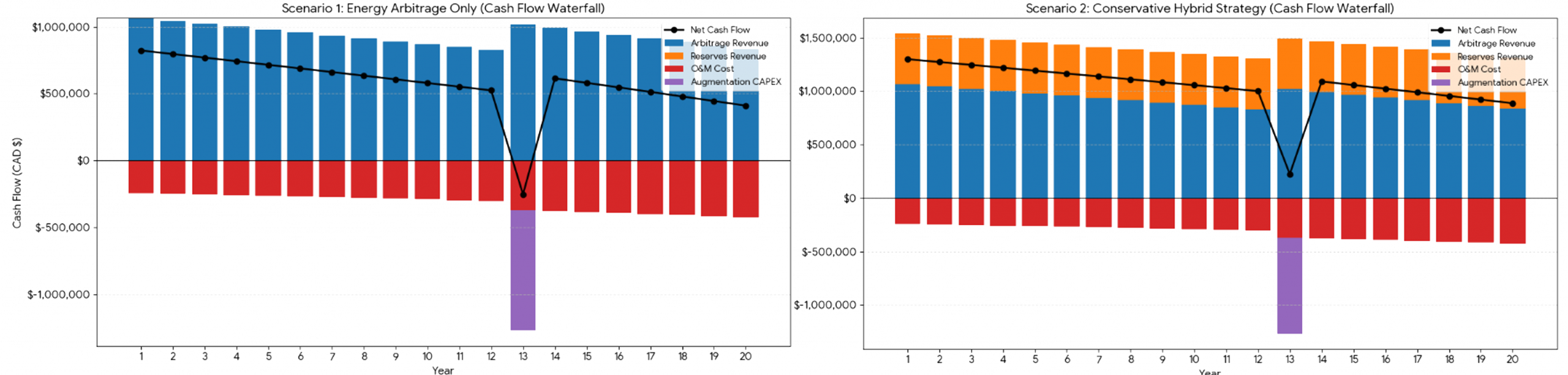

In Scenario A (Arbitrage Only), the project yields an IRR of only 2.52% and a Negative NPV of -$1.58M CAD. Despite a planned capacity augmentation in Year 13 to extend asset life, the revenue from daily energy price spreads is insufficient to offset the high upfront CAPEX and recurring augmentation costs. In contrast, Scenario B (Conservative Hybrid Strategy)—with limited (2-hour) participation in Operating Reserves—achieves an IRR of 10.69% and a Positive NPV of $4.35M CAD. By securing stable capacity payments ($64.29/MW/h), the project monetizes the battery’s availability rather than just energy throughput.

This strategic shift drives a net value swing of nearly $6 million. While the technical model identifies distinct climate-driven HVAC costs, these are financially eclipsed by the robust revenue stability of the “Speed Premium,” confirming that reserves determine economic viability for North American utility-scale BESS.

Discussion and Conclusions

This project demonstrates that sustainable profitability for utility-scale BESS in North America cannot be achieved through arbitrage alone. Even with favorable pricing periods, arbitrage revenues are too inconsistent and degradation-intensive to support long-term financial performance. Integrating Operating Reserves fundamentally changes the economics: reserve payments are stable, degrade the battery minimally, and provide the dependable revenue floor needed for investment and financing. Augmentation at the 75% SOH threshold further preserves long-term energy delivery and protects revenue. Overall, the model shows that BESS must operate as reserve-first assets, with arbitrage serving as secondary upside rather than a primary strategy. This approach aligns technical realities with financial viability.

Contact

Di Wu(Max)

Email: max.wu90@foxmail.com