Reading about Financial Accounting Fraud has led me to thinking about a concept that I’ve encountered earlier: window dressing.

Nope, it is not the kind of window dressing above that you’re thinking of. It is this kind:

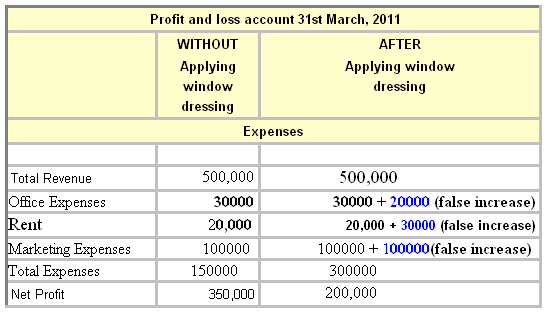

Window dressing is basically the “legal manipulation” of a firm’s financial data to make it look more appealing and flattering, according to the country’s laws. It is used for many reasons, including, but not limited to: showing the firm as profitable and sustainable, improving the liquidity position of the firm, showing less liabilities, mainly to impress and attract investors, financial lenders, and employees-mostly managers.

But then, what makes window dressing different from financial statement fraud?

Financial statement fraud is intended misrepresentation of the financial position of a firm in order to deceive and manipulate the users of financial statements. It is seen that financial statement fraud is making major changes to the figures, whereas window dressing is making minor changes that heavily impact the firm’s image. Still, what makes window dressing legal while financial statement fraud illegal? One thing is for sure, in my opinion, is that for both, it is a matter of being unethical towards stakeholders, who deserve to know of the actual financial position and performance of the firm.

http://www.scribd.com/doc/19470942/Window-Dressing

https://www.cga-pdnet.org/Non_VerifiableProducts/ArticlePublication/FinStatFraud/FinStatFraud_p1.pdf

Recent Comments