In human history, automobile bring a great convenience to everyone daily life. With the great benefit that modern society provided, we now need to rethink about our driving behavior and fully utilize our traffic system. Traffic Congestion is and always is a big headache that every modern society developer. No matter it is in China, US, UK or Canada.

A revolutionary plan has been carried out in EU, both Netherland and Germany are planning to apply the Meter Plan. The originally idea of using GPS technology to measure automobile moving distance comes from Netherland. Unfortunately, as 2010 new election in Netherland, the GPS meter plan was put on the shelf. New elected Netherland leaders use the term “tax burden of people” to describe this revolutionary technology. But actually, using GPS meter plan has several advantages. The first one is cutting the necessary cost for taxpayer.

I know, this sounds ridiculous. How come the meter plan will cut the cost of driver?

In fact, GPS meter plan will decrease the average cost of driving. As GPS meter system directly measure distance of driving and bill the car owner, this provides a more justified basis to collect the toll. In another words, not everyone have to pay the same toll. Moreover, GPS meter system will be a prefect substitute of registration fee or any other taxes for controlling the traffic. In the country of China, most of provinces still keep the administration team to collect the bill. After apply this new opportunities will substantially decrease cost of maintaining road.

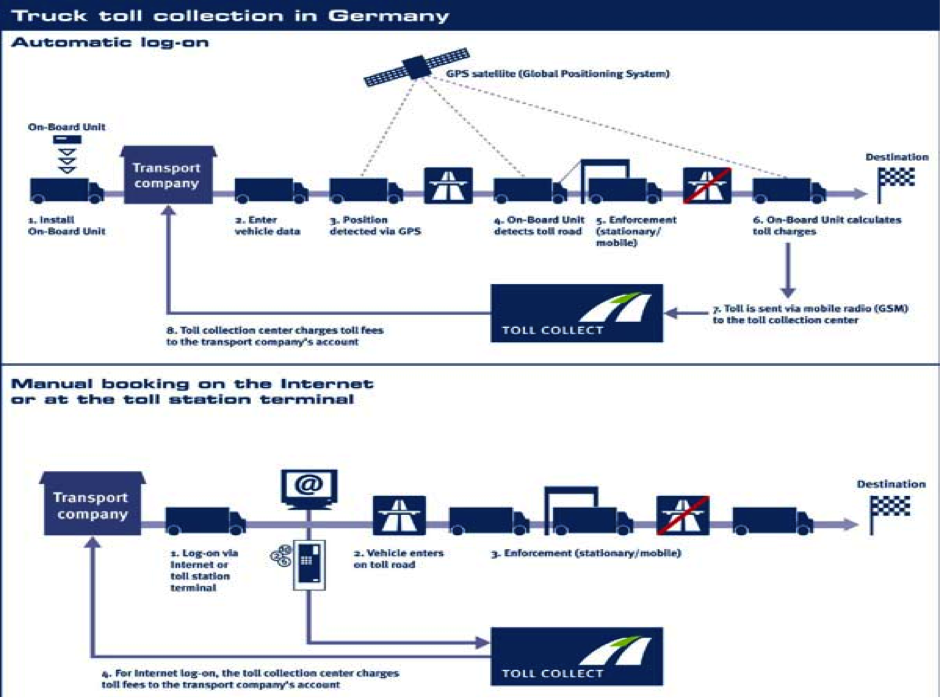

In Germany, the name of this project is “LKW-MAUT Electronic Toll Collection System”.

Two main services to collected the toll:

“ On Board Units (OBU) or Manual payment terminals, OBS work via GPS and the on-board odometer as backup to calculate how far the Truck have travelled by reference the digital map and GSM to authorize the payment through internet or wireless link.

Manual payment is for those trucks without OBU, there will be over 3,500 toll payment terminals at motorway service stations or rest areas where driver can enter the details of their journey.” [1]

Here is the diagram illustration about how this system works:

Of course, there is an administration team to enforce this new toll system. 300 cars and 540 officers formed the Federal Office of Freight. Those cars were equipped with high resolutions camera, Dedicated Short Range Communication system and IR detection system. In one sentence, those administration teams will enforce the new toll system, collected the evidence and stop the violation behavior.

The Coverage of Toll System:

Germany new toll system only covers the trucks. There are some hidden issues to explain why these systems only cover trucks.

- Privacy: One of the biggest drawbacks of this system is GPS will allocate your position whenever you go. Privacy issue is a big headache for the program developers. This drawback directly influences the public support for this toll system. However, from my perspective, this concern is unnecessary as modern technology could easily track people’s location by checking cellphone, Internet connecting point.

- Capacity: Now the performance of this new system is well. LKW-MAUT system can monitor about 1.3~1.5 million trucks. Now, the registered driver is approaching to 1 million. However, the total number of cars in Germany is about 56 million. [2] It will be too ambitious to apply this system to all type of cars. The whole system will face a lot of challenges both form public and current technology.

The Environmental and Distribution impact of LKW-MAUT

First thing I need to emphasis is LKW-MAUT was not only tax on distance truck driver moving but also tax on the carbon emissions.[3] From my perspective, this is a brilliant idea in design phrase. As it serve for the purpose of changing driving behavior and cut for the carbon emission. This tax will also encourage people to adopt oil-efficient technology. The reason is quiet simply, as the marginal cost of emitting growing higher, people have the incentive to adopt greener technology in order to maintain profitability.

Moreover, I do believe this a revolutionary technology. As drivers were taxed by the distance they drive and their carbon emission, drivers who drive less do not need to pay the same amount of toll or registration fee. This is a better platform compared to current one, as people are who drive for a longer time and longer distance share more responsible of traffic congestion.

The distribution effect of LKW-MAUT is obvious, logistic company have to pay more under new system. Citizens or taxpayers are the beneficiaries as they could pay fewer tolls. Poor people are not touched by this new system yet. But if the coverage of this system were expended, people who cannot afford the cost will drive less. Poor people will live near to urban area, public transportation system will expended as more people are using this travel system.

The performance and Effectiveness of LKW-MAUT:

From my perspective, the performance of LKW-MAUT is very well.

There are two indicators:

- Constantly updating the monitoring system

Germany administration teams are trying their best to close the loops of this system. Companies’ undated new digital maps increase the accuracy of satellite system. “In 2007 Toll Collect extended the scheme onto major trunk roads in Germany to prevent what was seen as toll avoidance by some truck drivers.”—- (Roadtraffic-technology.com)

- Number of registries driver:

The Number of driver is increasing. Now is approaching to 1 millions. This indicates new toll system is become popular in Germany.

The effectiveness of LKW-MAUT

LKW-MAUT effectiveness is mainly dependent on enforcement team. As the design of this system is the best option for us, truck drivers are taxed by the distance and carbon emission. The enforcement team is the key to make sure this system is operated as its designers’ idea.

In Conclusion, I do believe LKW-MAUT is a very good system to solve the traffic congestion. As GPS tolling system still in its early age, there are still many obstacles in its implementation. Privacy concern for the public is one the key problems need to be solved or compromised in the future.