Recently much of my work has been revolving around building a trading strategy that optmises on the mean reverting behaviour of the stock market.

This blog post is to give insights into some of the interesting tools i have had the pleasure of working with.

Ornstein-Uhlenbeck process

dt + \sigma dB_t")

with constants

The parameter

Pairs Trading example

The pair of assets are selected to form a mean-reverting portfolio value. In addtion, one can adjust the strategy ")

under the model.

with the constant

the conditional probability density of

Maximising the average log-likelihood over

")

")

think of }")

}")

}")

Log-likelihood function:

Using the observed

Example

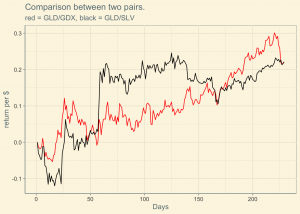

Using the price data from August 2011 to May 2012 (n = 200, ∆t = 1/252), for GLD-SLV and GLD-GDX.

Shown above is the performance of a portfolio that has

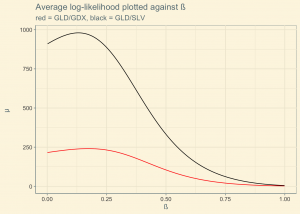

The above chart shows the comparison between the two pairs trading examples using the optimised beta levels obtained through the use of the model.

Citations: Optimal Mean Reversion Trading with Transaction Costs and Stop-Loss Exit paper [Tim Leung and Xin Li.]