Kevin Milligan

Professor of Economics

Vancouver School of Economics

University of British Columbia

Prepared Comments on Tax Planning for Private Corporations for Standing Committee on Finance

September 26, 2017

Ottawa, ON

I’d like to make two points this morning. First, I want to talk about the goals of this reform package. Second, I will discuss implementation.

A main goal of this reform is to push toward neutrality. A neutral tax system is one where people make the same business decisions in the presence of taxation as they would in a world without taxation. With a neutral tax system, the government has the lightest possible touch on the economy. Business decisions are made on business merits, and not pushed one way or the other by taxes.

The current system falls short of neutrality in many ways. One example is to consider a hard-working unincorporated person: someone with a truck, a hammer, some skills, and a passion for work. We want her to be able to start a business without the costs and hassle of incorporation. By loading tax benefits onto those who organize their businesses as corporations, we lean against people who want to work just as hard for their families, but in an unincorporated business. This has real costs to our economy.

Now, some words on implementation. Many tax practitioners have raised concerns about how some of the proposed tax measures may be implemented. As one example, when dividends are paid to family members, there are concerns about the accounting and keeping of records to support a claim for ‘reasonableness.’ There are many other examples.

In my view, some of these concerns hit the mark and they must be treated seriously. After the consultation period is complete, I think it is important for the Department of Finance and the Minister to provide a wide-ranging and thorough response to these concerns. I’m sure they are now working hard at this important job, and I look forward to hearing their responses.

But, we should not stand frozen from action because of concerns about transitions and implementation. Tax changes always require adjustments. To fret too much about adjustments simply resigns ourselves to the status quo, and Canadians deserve a tax system that works better than the one we have today.

Notes prepared for the Canadian Tax Foundation conference “Tax Planning Using Private Corporations: Analysis and Discussion with Finance,” held in Ottawa on September 25, 2017.

“The system would neither encourage nor discourage the retention of earnings by corporations”

This was the goal set out by the Carter Commission 50 years ago for the integration of the corporate and personal tax systems.

“…neither encourage nor discourage the retention of earnings by corporations”

The goal embodied in that quote is neutrality. Neutrality is at the centre of the concept of economic efficiency. A neutral tax system means that people make the same decisions in the presence of taxes as they would in a world without taxes. Neutrality means that government has the lightest possible touch; business decisions are made on business merits, not pushed one direction or another by tax considerations.

Is neutrality a lofty idealistic academic goal? Of course. Along the road to any goal, we need to confront the concerns of on the ground reality. Concerns of administration. Of complexity. And of practical issues of tax law. These factors can and should determine how far down the road we go toward this goal.

But let us start first with deciding down which road to travel. I think this benchmark—“neither encourage nor discourage”—set out by Carter is a good one. Over the next few minutes, I will explain why I think this is a good goal, then explore how good a job these proposed reforms do in achieving this goal.

What is integration?

Integration means that tax at the personal level should reflect tax already paid at the corporate level.

Put differently, all paths for a $ from “profit to pocket” should bear the same tax.

If integration holds, there should be no financial gain from readjusting the location of savings. Again, recall Carter:

“The system should neither encourage nor discourage the retention of savings by corporations.”

Why integration?

Integration supports neutrality: we want people making the same decisions as they would without taxation. This is a free-market goal and the literal economic definition of an efficient tax.

Firm owners decide to save inside the firm for a variety of reasons: retirement, maternity leaves, ‘buffer’ savings, saving for a future reinvestment. This is all fine, but the tax system should neither favour nor disfavor any of these choices. These decisions should be made on business merits, not pushed one way or the other by taxes.

It is useful to remember the reason we have the Small Business Deduction. The introduction of the SBD was explicitly meant to facilitate active investment. That’s the reason laid out in the 1971 budget speech by Edgar Benson.

If a corporation employs the tax savings that result from the low rate for non-business purposes, such as Portfolio investments, a special refundable tax will be imposed to recover the low-rate benefit.

We intend that the small business incentive be available only to Canadians and that it encourage Canadian ownership of our expanding businesses.

Ways Current Integration Falls Short

The current system of integration falls short of an academically pure neutrality in a variety of ways:

It’s notional; doesn’t reflect actual taxes paid.

One national gross-up rate.

Tax-exempts like RPP/RRSP can’t claim DTC.

Capital gains rate currently ‘too low’ compared to dividends/wages.

Firms claiming SBD have a ‘head start’ deferral advantage for saving.

The current proposals really only address the last of these. The aim here is not perfection, but to try to make an imperfect system a bit less imperfect. That’s a fine goal.

Do proposals improve integration?

I will present some analysis of the proposals on passive income. I focus on high-bracket investors for a few reasons:

High bracket investors are much more likely to have large passive portfolios.

Current system imposes a high flat tax on passive income, so low/mid bracket investors are already disadvantaged. Not clear it makes financial sense for them to save inside a corporation under the status quo.

But, it should be acknowledged that the proposals will make saving inside a CCPC even worse than the status quo for a low- or mid-bracket investor.

The current system is ‘over-integrated’, meaning that the credits given for tax paid inside the firm are too high. The proposed remedy is to remove the refundable dividend tax on hand (RDTOH) notional amount that is currently included when dividends are paid out.

Some have argued that the resulting tax rate on passive income inside the firm is excessive. But, any analysis needs to look at the whole flow of income from beginning to end. Inside the firm the taxation of the principal is very light to start, so the heavier taxation of the accruing income balances things out.

I will offer two pieces of evidence on integration under the current and proposed system.

My analysis starts with $100 of pre-tax active business income and watches what happens when it is retained inside the firm or immediately distributed over a 10 year period. Under the status quo, the individual is about 10% better off saving inside the firm as outside the firm. With the proposal, there is virtually no difference for saving inside and outside the firm.

This can vary a bit depending on time horizon and the mix of assets held. However, in my analysis the reform is fairly successful at removing the current deferral advantage of saving inside the firm.

The second piece of evidence is simple observation. If a system is properly integrated then, as per Carter, there should be neither advantage nor disadvantage from retaining earnings.

I observe the following. The financial planning industry in Canada makes a strong pitch to firm owners that there is a deferral advantage for saving in CCPCs. This pitch is not hard to find—a simple google search reveals dozens of examples.

If there is a deferral advantage, then the system is not currently properly integrated. If you claim there is no deferral advantage, then the ubiquitous pitch made by financial planners is wrong. I do not think this pitch made by financial planners is wrong. There is a current deferral advantage and that means the system today is not properly integrated.

How much do the proposals matter?

The last point I’d like to make is to emphasize the scale of the impact of the reform. I will do this in two ways—first with a simple example then a slightly more involved example.

First, the simple example. Imagine $100,000 in a passive portfolio paying 5% interest income. The change in tax for an Ontario high bracket tax payer can be calculated as:

There is $5,000 of passive income.

RDTOH on the $5,000 is 30.67%, or $1,534.

But, this is taxed as non-eligible dividend income. 45.3% effective rate for Ontario high bracket

So, RDTOH is worth $838 after tax if flowed through to the individual immediately.

This is <1% of the total value, but does eat up 17% of the return.

After 10 years, this can affect terminal value of the portfolio by 8-15%.

Is this large or small? That’s in the eye of the beholder, but I think it’s important to keep the scale in mind.

Now the slightly-more-involved example.

Imagine someone saving $33,333 per year for three years. This could be for the purposes of a reinvestment in the firm, a maternity leave, or for eventual consumption purposes outside the firm.

Imagine again that the savings earn interest income at 5% per year. This income is taxable each year as passive income. Here is what the account looks like at the end of three years.

The balance is $105,067. There is also a balance in the RDTOH account of $3,118. This has an after-tax value of $1,705.

Passive investment example

Two points to make.

First, for money reinvested in the firm there is no change to cash flow. There is no less cash available for a maternity leave or a reinvestment. The RDTOH account is notional, so it only affects cash once there is a dividend paid eventually.

Second, because of the removal of RDTOH, the change in the after-tax value of the portfolio because of the reform is $1,705, or 1.6%.

So, for those using a passive portfolio to save short-term within the firm, there is no change to cash flow and a fairly small change to the portfolio value.

Concluding thoughts

“The system would neither encourage nor discourage the retention of earnings by corporations”

My job here, as an economist, is to help us figure out what goals to set for the tax system. I think this goal, as laid out in the Carter Commission, is a sound one. At its core, integration and neutrality mean that business decisions can be based on business merits.

Of course, in deciding how far to go toward any goal, we need to weigh the costs and benefits. There are lots of important challenges that await.

Transition: how grandfathering will work.

Inter-company shareholdings and investments in startups.

I’m sure we will hear more today!

I’d like to emphasize that these concerns are serious. If there are problems, we need to see if Finance can fix them. If they can’t be fixed, certain elements of the package will then need to be reexamined. But, these issues are much more the purview of the lawyers and accountants among us than the economists. I have a suspicion you won’t need my encouragement to speak up on this as the day proceeds. I look forward to hearing what you have to say.

Other speakers have covered the details of the proposed reform package in detail, so I will just summarize it briefly. The proposed package contains three measures.

Cutting back on the ability of business owners to “sprinkle” income to other family members.

Imposing heavier taxes on passive portfolio investments inside a corporation.

In my time here, I’m going to make three substantive arguments about the goals of the tax reform, and assess this private corporation policy package as a whole.

The three substantive points are about efficiency, entrepreneurs, and equity.

Efficiency and Neutrality

The core aim of the reform is to restore neutrality to those conducting business inside vs outside a corporation. It’s worth spending some time to understand why this is important.

At the core of the economic model of taxation, we use as a benchmark the activities people would undertake if there were no government and no taxes. When we introduce taxes to the model, we compare what people do to what they would’ve done in the absence of taxes. The choices made without taxes are our ultimate benchmark.

The ideal for a tax system is neutrality. Neutrality means people choose the same activities with or without taxes. In other words, a neutral tax system is one where the government isn’t pushing economic activity one way or the other; a neutral tax system has the lightest possible touch of government on the economy. That’s the goal.

This concept of neutrality is central to the motivation for the current reform package. To apply this concept, we don’t want to give tax advantages to those who run their business as a corporation compared to those who run their business as unincorporated, or to those who save inside versus outside a corporation.

The reform aims to pull back on the tax advantage of incorporation. Incorporation is appropriate in many business circumstances, but the incorporation decision should be made on the business merits, not because of tax incentives. We as a society don’t have incorporation because we want people to give people tax advantages. We don’t have incorporation as a back-door way to give family-based taxation to a subset of Canadians. We don’t have incorporation to provide a parking place to put your retirement portfolio. You can argue that family taxation and retirement savings are good things, but that’s not what a corporation is for. The role of a corporation is to facilitate productive investment to grow the economy and produce better jobs.

Productive investment should be the focus, not loading tax savings into one particular way of organizing a business.

This is the basic efficiency case for a reform that moves toward neutrality.

Entrepreneurs

The future of our economy is built by investment decisions made today; our future prosperity is determined by the accumulated impact of each one of those investments. We want new ideas, new firms, and new jobs to be grown right here in Canada, and the job of policy is to make sure that happens.

Is there a case for helping small business? Ted Mallet, the economist for the Canadian Federation of Independent Business argues there is.[1] He provides some good examples:

Large firms have economies of scale in dealing with government regulations.

Internationally active firms can lower cost of capital through international tax arbitrage.

While I think Mallet makes a good economic case for helping out small business, it’s not clear to me the existing Small Business Deduction (SBD) is the right way to do this.[2] The SBD targets small firms; we want a system that targets new and growing firms.

If our goal is helping entrepreneurs, one attractive option put forward by Chen and Mintz introduces a system where every firm can immediately expense a certain amount annually, rather than deferring the depreciation deductions.[3] This gives an advantage to smaller firms, and the advantage is directly targeted where we want it: incentives to grow investment.

While it is useful to think about bigger potential reforms, we also must address the reform package currently on the table.

Do the three tax measures currently on the table spur entrepreneurship? Are these measures effective subsidies for what we want to achieve?

The ability to sprinkle income does not reward those with good ideas. Sprinkling is not a reward for innovation, investment, or job growth. Sprinkling rewards those with a certain family structure. As for passive portfolio income, by its literal and legal definition it is the opposite of active investment in firm activities. We want productive investment in firms; we want to encourage entrepreneurial activities. It is very hard to see the link between income sprinkling and passive portfolio taxation and innovation and entrepreneurship.

I think the government can and should do more to encourage entrepreneurship and growth through the levers of the tax system. We have much better ways to encourage entrepreneurs than income sprinkling and subsidizing passive investment.

Equity

A major consideration for the politics of taxation—and the economics of taxation—is to figure out who is affected by these tax measures.

These tax measures strongly and obviously impact high earners much more than anyone else. But before I get to the facts, let me start with three caveats.

The compliance burden of some measures may hit many regular small businesses. I hope to hear some creative ideas about how to lower the compliance burden of achieving the reform’s goals. But ultimately, the final package has to take into account whether any additional compliance burden is justifiable.

Poorly written draft legislation might rope in too many regular small businesses. I hope Finance is listening and offers fixes to problems that have been raised.

You can construct special cases showing someone as low as $70,000 per year might have a small impact. We should take note, but not generalize from these special cases.

In my view, these reforms have their largest impact on high earners.

First, take the case of income sprinkling. The gain to shifting income across taxpayers within a family is driven by the difference in tax rates. If the main operator of the business is in a middle tax bracket, the gain to splitting income is quite small. As the gap in the tax rate between the main operator and the other family members grows, the gain from sprinkling income grows.

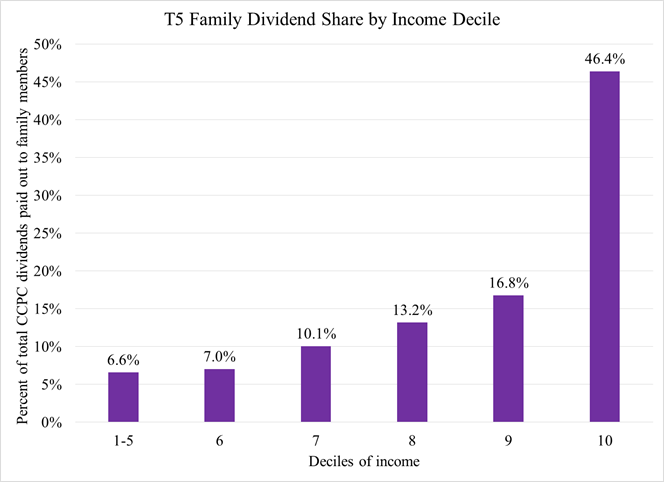

The data on dividends provided by Michael Wolfson and Scott Legree makes this very clear.[4] If you put Canadians into ten decile bins and observe who is paying out dividends to family members, only about 6 percent is paid out from the bottom 5 deciles in total. In contrast, the top decile of income is the source for 46 percent of total dividends paid out to family members. Note that this is an understatement of the ultimate tax impact, since the actual tax dollars would be even more skewed than the income shown in this analysis. The tax dollars are more skewed because the tax gain to income splitting is much bigger for higher earners for a given dollar of income since the gap between their tax bracket and the dividend recipient’s bracket is on average larger.

Source: Wolfson and Legree (2015)

Second, let’s look at the taxation of passive portfolios. All working Canadians have access to the Registered Retirement Savings Plan / Registered Pension Plan / Tax-Free Savings Account system. If you’re a small business owner looking to save for retirement, in most circumstances you can do as well and likely better in an RRSP or TFSA than saving inside a private corporation.[5] So, the people for whom a private corporation starts to make sense are those who have more savings than can fit in the regular RRSP/RPP/TFSA system.

Of note, RRSP room for 2017 is $26,010 which covers earnings up to $144,500 if one contributes the maximum of 18 percent of earnings. Moreover, in 2015 23.1 million Canadians had a total of $909 billion in carried-forward RRSP contribution room, meaning they had RRSP space available.[6]

As a final consideration, the special tax rate that applies to passive income inside a corporation is a flat rate set to approximate the top tax bracket outside a corporation. For 2017 in Alberta this special rate is 50.67%. Since it is a flat rate, people in middle or lower tax brackets see an advantage for saving outside a corporation compared to high-bracket investors. This is the current situation.

So, while I am aware of no public data on the distribution of the $26 billion of passive investment income from CCPCs, it would be very surprising if many low or middle earners are currently making use of what is for them an expensive and tax-inefficient location for their savings.

To sum up, it is possible to construct a case that middle earners could bear some financial impact of these reforms. But the evidence and logic is quite clear that the impact of the proposed private corporation tax reform will fall most heavily on higher earners.

The path forward

To put a framework on this analysis, I propose separating policy advice into two piles.

The first pile is the “fantasy tax reform” pile. These are ideas that are outside the current political constraints.

Some examples:

We should have a big-bang tax reform (Carter 2.0).

We should just get rid of SBD.

We should lower top tax rates substantially.

We should have the family as the tax unit.

As academics and policy thinkers, it is our job to think outside current political constraints, so I welcome those offering and defending bold ideas of how we can do things differently. This is vital; that is why we sit in our “ivory towers”; to think things people in the hot house of every-day politics don’t dare to think in a particular moment.

The second pile of policy advice is to evaluate what’s on the table now. What is actually possible given current political constraints?

For this kind of policy advice, we need to compare any policy package not against the “fantasy reform” alternative, but against the status quo. Does a reform package improve us compared to doing nothing?

While offering “fantasy policy reform” advice is useful, we can’t hide from analyzing what is on the table now and comparing it not to an ideal, but the status quo.

So let me use this framework to analyze the current policy.

Does this reform meet my own personal fantasy tax reform checklist? Not really. I can see the benefit of a big “Carter 2.0” tax commission that plans our system on a rational basis for the 21st century. I think the existing small business deduction should be replaced with something better targeted at new and growing firms. The Finance package of reforms is clearly a patch on an imperfect and messy existing system.

But to the 2nd question, does this reform improve on the status quo? I think this reforms heads us in the right direction, on both efficiency and equity grounds. To merit full support, I think it is feasible and necessary to expect the Minister of Finance to address the following items when the final package is put together following the consultation period.

Administrative burden; e.g. easier accounting for ‘connectedness’ for Mom and Pop shops.

Problems with the draft legislation: Lots of examples have been floated that may lead to bad tax outcomes. Are these examples correct? Can they be fixed with better legislation?

Solid and feasible plan for transition: can the passive income reform legislation meet the goal without too much complexity?

Do more for entrepreneurs and startups. Turn the new revenue around within the small business envelope. If the Minister is serious about encouraging entrepreneurs, show it.

[1] Ted Mallet (2015), “Policy Forum: Mountains and Molehills—Effects of the Small Business Deduction,” Canadian Tax Journal, Vol. 63, No. 3, pp. 691-704. [link]

[2] The Mirrlees Review in the UK argued that there may be a case for using fiscal tools to help small business, but those tools should be targeted at the source of the market failure rather than a broad-based rate cut. See Claire Crawford and Judith Freedman (2010), “Small Business Taxation,” in Stuart Adam, Tim Besley, Richard Blundell, Stephen Bond, Robert Chote, Malcolm Gammie, Paul Johnson, Gareth Myles, and James M. Poterba (eds.) Dimensions of Tax Design. Oxford: Oxford University Press. [link] Also, the recommendations of the Mirrlees Review can be found in James Mirrlees, Stuart Adam, Tim Besley, Richard Blundell, Stephen Bond, Robert Chote, Malcolm Gammie, Paul Johnson, Gareth Myles, and James M. Poterba (2011), “Small Business Taxation,” Tax by Design. Oxford: Oxford University Press. [link]

[3] Duanjie Chen and Jack Mintz (2011), “Small Business Taxation: Revamping Incentives to Encourage Growth,” School of Public Policy Research Papers, Vol. 4, Issue 7. [link]

[4] Michael Wolfson and Scott Legree (2015), “Policy Forum: Private Companies, Professionals, and Income Splitting—Recent Canadian Experience,” Canadian Tax Journal, Vol. 63, No. 3, pp. 717-738. [link]

[5] I worked out a specific case in calculations available through my UBC blog here. Financial planning expert Jamie Golombek works through some more sophisticated cases here. Of course, individual circumstances vary so universal statements about the tax efficiency of different investment strategies are difficult.

[6] See CANSIM table 111-0040. There were 26.4 million taxfilers in 2015. Some of the 3.3 million (representing 12.4% of the total) without carryforward room were ineligible to contribute (for example someone over age 71), while others had used up all their available room.

This blog post assembles information I’ve provided to the public on the proposed changes to the taxation of private corporations. The discussion document from the Department of Finance is here. My disclosure is here.

The links below all work right now (Sept 2017), but some of them may go 404 as time passes.

I will be speaking at two academic conference in the next few weeks on the topic of the proposed changes to the taxation of Canadian-controlled private corporations (CCPCs). In preparation for these conference, I have prepared some spreadsheets to explore how the mechanics of the proposals should work. I have shared these with the public here, and I welcome feedback at kevin.milligan@ubc.ca. My disclosure documents can be found here.

The proposals can be found on the Finance website here:

In this blog post, I explore three scenarios for the taxation of passive portfolios. The reform also changes rules about ‘sprinkling’ income to family members, and converting income into capital gains. I don’t discuss those issues here in this blog post.

The aim of the reform to passive portfolios is to ensure people with portfolios of taxable assets face the same tax rates whether they choose to save inside or outside the firm. We economists call this ‘neutrality’. Neutrality is desirable because it allows people to make decisions based on the business merits, rather than having their decisions distorted by taxation. That’s both efficient and fair. Moreover, the reason societies have corporations is to facilitate productive investment, not to offer tax savings to those with large passive portfolios.

So, I defend as economically sound the aim of the reform to strive for neutrality. But will the reform actually achieve neutrality? One important question is whether the officials at the Department of Finance got the math right. It is this question I address with my spreadsheets and scenarios below. Another important question is whether the legislative/legal/accounting approach taken by Finance is the most effective. I leave that question to others.

Before getting to the scenarios, let me start with the bottom line:

In my view, Finance got the math right with their proposals on the taxation of passive portfolios.

Scenario 1: The (Incorrect) Immaculately-Conceived Principal

This scenario compares the taxation of $100 of passive interest income in various tax locations:

Personal (taxable)

Personal (TFSA)

Inside a private corporation in the status quo

Inside a private corporation under the proposal

My view is this is the wrong way to approach the question. Why? Because it doesn’t account for how the principal that generated the investment income was taxed. For savings inside a CCPC, the initial principal is taxed very lightly, so those savings get a large ‘head start’ compared to savings outside the CCPC where the principal faces initial heavy taxation. This is apples-vs-oranges.

For this scenario, it’s as though the principal were ‘immaculately conceived’ and its taxation can be ignored. I think this is wrong. Why do I present an incorrect scenario here? Because I’ve seen many analyses from reputable financial planners that use this approach and I wanted to see that I can replicate it and understand it.

In the spreadsheet, I can replicate the claim being made that the effective tax rate on investment income is 73%. But, I contend that the basis for this calculation is wrong–they are assuming the principal is immaculately conceived.

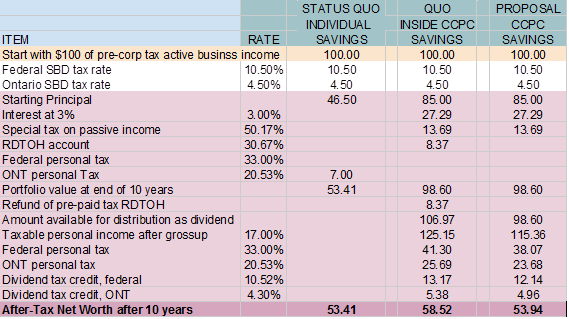

This is the correct way to approach the question. It starts with apples-vs-apples. $100 of pre-tax corporate active business income for all cases. I compare the same four cases as Scenario 1, using a high-bracket Ontario investor and a one-year time horizon. The main result is in Row 25. Savings on personal account yield $47.15, and in a TFSA yield $47.90. In the status quo, inside a CCPC the yield after one year is $47.63. Under the proposed reform, RDTOH is removed, so the one-year yield falls to $47.20.

There are several important points here:

The aim of the reform is neutrality for savings inside and outside the firm. The success in meeting this goal can be learned by comparing D25 with J25. They are very close. They are not exactly the same because the dividend tax credits and gross-up rates lead to small discrepancies.

The proposed change under the reform is to no longer allow the RDTOH refund. This leads to the differences between columns H and J. The one-year difference is 43 cents, or 0.43% of the initial $100 in earnings. this strikes me as quite small.

Of note, the TFSA in this example does better than any other savings location. If you had dividends or capital gains income the advantage of the TFSA would shrink. This is important for the following reason: in most cases, it makes much more sense to invest through a TFSA or RRSP than inside a CCPC. Using a private corporation to house a passive portfolio really makes sense if you have exhausted TFSA/RRSP room. It is less clear why it would make sense to anyone with only a smaller amount of savings that could be housed in TFSA or RRSP. (But these scenarios do exist–for example Americans living in Canada face big tax issues with TFSA/RRSPs…..)

In the Finance discussion document, the key table for the taxation of passive portfolios is Table 7. They go about the calculations in a different way than I did in Scenario 2. It is a very useful check on my calculations to see if I can replicate their Table 7 result, and to see if it matches my Scenario 2 result.

Of note, the Notes to Table 7 state they are based on:

“simplified tax rate assumptions, chosen to remove small discrepancies that can arise due to imperfect integration of federal-provincial tax rates and differences between the top personal income tax rate that applies in each province and current tax rates on corporate passive investment income.”

In English, this just says that the gross up rate (117%) and the tax rate on passive investments (38.67%) are one-size fits all. They adjusted their Table 7 tax rates so that the numbers work ‘perfectly’.

I take a slightly different approach. I just use Ontario. So, I expect that my numbers will differ a bit, but the patterns of where taxes on savings are heaviest should remain the same.

In Scenario 3, I start with a one-year horizon. Of note, I get the exact same results as I did in Scenario 2. This gives me strong confidence I’m getting it right–I got the same answer using two different approaches. The answer is that saving through a CCPC yields a 0.43% per year advantage over savings in an individual taxable account.

Underneath, I do a ten-year investment horizon like in Finance Table 7. I find that saving inside a CCPC currently gives you a 5.11% advantage over a ten-year horizon. Finance Table 7 finds a 4.89% advantage. Under the reform, this advantage drops to 0.53% over ten years. Finance finds a 0.00% difference over ten years. The differences between my numbers and Finance are driven by the fact I use ‘Ontario’ and they use ‘simplified’ tax rates. So, I am very confident I can replicate Finance Table 7.

The lessons here:

I have independently replicated Finance Table 7.

The status quo gives CCPC savers about a 0.43% per year advantage over people saving outside a CCPC.

Over a ten-year horizon, the gain is 5.11% of the initial corporate earnings. Five buck on a hun.

According to p. 12 of the Finance document, there was $26.2B of passive income in 2015, so it doesn’t take much of a rate change to create a sizeable change in tax revenue. BUT, remember that the Finance document says they intend to ‘grandfather’ in existing CCPC savings, so any new tax revenue would only start phasing in through time.

Conclusions

The point of my spreadsheets and this blog post is to present an exploration of the taxation of passive investment income inside CCPCs. I hope this can contribute to public debate. I am interested to hear feedback at kevin.milligan@ubc.ca.

I have confidence in my ability to check on Finance’s math. In my view, Finance got the math right here. I do not have the professional capacity to judge whether Finance has the draft legislation correct. I leave that question to others.

UDPATE May 12th:Elections BC has announced a revision to the preliminary count in Coquitlam-Burke Mountain which moves the margin from BC Liberal +170 to +268. This has a pretty big impact on the simulation results because it makes it much harder for the NDP to flip this riding. I’ve updated the text and charts below to reflect this change.

—

The preliminary counts from the BC election on Tuesday May 9th resulted in an apparent seat count of 43 BC Liberals, 41 NDP, and 3 BC Green MLAs. Because of the tight partisan balance, there is much interest in whether this result will hold up when all the votes are counted–around 10 percent of votes made through absentee ballots have not yet been counted. In this blog post, I first clarify how absentee and other special ballots matter. Following that, I present an analysis of the probability of a change in the outcome tallied on election night. The main finding: there is a 1 in 4 chance that the 43L-41N-3G seat count from election night will change once all the ballots are counted.

Voting in BC

In BC in 2013, about 70 percent of voters place their vote in their designated voting station. Another 20 percent voted in advance. Both of these categories are counted on election night. However, there are six more categories of voters that provide another 10 percent of votes that are not counted with the preliminary count on election day. The BC Election Act lists all eight different categories of voting, which I produce below along with the 2013 proportions of each category and the relevant section of the Election Act.

Section 96 (69.9%): General Voting

Section 97 (20.3%): Advance Voting

Section 98 (0.8%): Voting at a special voting opportunity

Section 99 (4.3%): Voting on election day, but in a different voting area

Section 100 (1.81%): Voting on election day, but in a different electoral district

Section 101 (0.6%): Absentee in advance

Section 104 (2.0%) Voting in District Electoral Officer office

Section 106 (0.4%) Voting by mail

The bottom six categories are to be counted between May 22nd and May 24th–two weeks after election day. In 2013, these six categories totaled 9.8% of total votes. Only a small fraction of this is the mail-in ballots. Most of the 9.8% is just people who voted in a polling station different than the one printed on their voting card–perhaps somewhere located more convenient to work, school, or family obligations. For 2017, Elections BC announced that the absentee total is 176,104 ballots.

Impact of Final Vote Count

The preliminary vote count on May 9th led to several close results–four districts with a lead less than 300 votes. (See all results in a google document here.) In both the 2009 and 2013 elections, two results ‘flipped’ between the initial count and the final count. If some districts flip in 2017, the partisan balance of the legislature may change. For this reason, there is strong interest in the likelihood of different seat-count scenarios. Below, I present simulations that aim to inform the public about these likelihoods.

First, let me list the five closest districts, the current lead, and the party currently in first place.

Courtenay-Comox: 9 votes, NDP

Maple Ridge-Mission: 120 votes, NDP

Coquitlam-Burke Mountain: 268 votes, BC Liberal (revised from +170 in initial preliminary count)

Richmond-Queensborough: 263 votes, BC Liberal

Vancouver-False Creek: 560 votes, BC Liberal

When the final counts are announced, there will be extra votes for all the major parties. If the proportions of the absentee ballots differ from the proportions of the preliminary count, there will be a final count ‘bonus’ for one party or another. Some of the close races listed above will flip if these absentee ballot bonuses are large enough.

We cannot observe the absentee ballot bonuses for 2017 yet. To get a sense of whether the bonuses are likely to be large enough to flip any districts, I turn to the results of 2013. With the 2013 data, I calculate the absentee ballot bonus for each of the BC Liberal and BC NDP candidate for each district. These are measured as the gain in the percent vote share between the preliminary and final votes. So, if the BC Liberal candidate received 40.1% in the preliminary count and 40.4% in the final count, this scores as a +0.3% bonus.

For BC Liberals, here is what these absentee ballot bonuses looked like in the 85 districts in 2013.

Mean: -0.36%

10th percentile: -0.66%

25th percentile: -0.48%

50th percentile: -0.36%

75th percentile:-0.12%

90th percentile:+0.04%

For the BC NDP, here is the same information for the 85 districts in 2013:

Mean: +0.23%

10th percentile: -0.07%

25th percentile: +0.05%

50th percentile: +0.27%

75th percentile:+0.38%

90th percentile:+0.55%

So, there appears to be a systematic lean toward the NDP in the absentee ballot bonus. Why is that? It might result from a more energetic ‘get out the vote’ effort by the NDP. Or, it might result from a different selection of voters who make use of the absentee ballot opportunity. Either is a plausible explanation.

These kinds of absentee ballot bonuses matter. In 2013 for example, Coquitlam-Maillardville swung from +111 for the BC Liberals in the preliminary count to +41 for the NDP in the final count. This was a swing of 152 votes (or 0.70% of the final total vote count). So, the kind of swings necessary to move some 2017 districts are not impossible.

Here’s how I proceed to examine the sensitivity of the 2017 preliminary results to the absentee ballot bonuses.

For each close district in 2017, I take the BC Liberal and NDP vote share. No seats involving the BC Greens are close enough to matter.

I then assign an absentee ballot bonus to both of these parties in that 2017 district, drawn randomly from the set of 85 districts in 2013. Both the BC NDP and BC Liberal bonus is taken from the same 2013 district for each draw.

This is repeated across all 5 close districts for 2017.

I add the BC Liberal bonus to the BC Liberal initial vote share, and the same for the NDP.

I then see if the result flips and add up the final seat count for each party.

Repeat this 1 million times, record the results.

What can go wrong with this method?

The 2017 distribution of absentee ballot bonuses may be different than 2013.

The particular districts in play in 2017 may have idiosyncrasies not incorporated into the simulation. For example, Courtenay-Comox has a military base and the BC Liberal candidate served on that base. This kind of special situation is not incorporated into the simulation, since the simulation assigns a ‘generic’ absentee ballot bonus to each party.

The absentee ballot bonus may be correlated across districts. The simulation described above assumes that each 2017 district gets an independent draw from the 2013 distribution of bonuses. Instead, it is possible that there may be a province-wide swing in favour of one party or another. That is, a correlated bonus. I account for this by presenting an alternative simulation that draws one bonus from the 2013 distribution and applies that one bonus to all the 2017 districts. This can be considered a polar case of perfect correlation to be compared to the uncorrelated case presented first.

Here are the results. First, for the uncorrelated case in which each 2017 district gets an independent draw from the 2013 absentee ballot bonuses.

BC 2017 Election Simulations, Uncorrelated Case

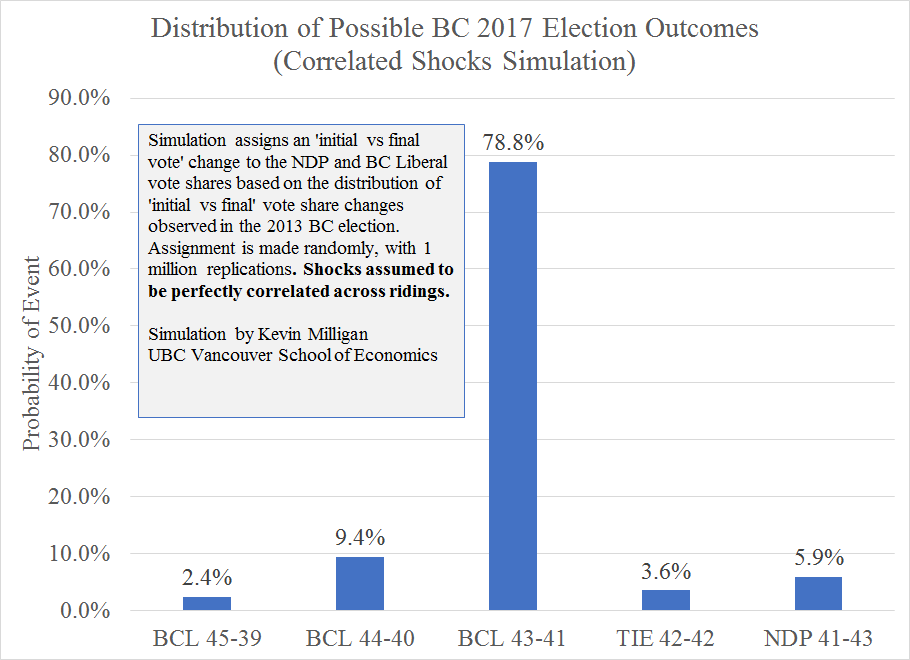

Next, here is the correlated case, in which each 2017 district gets the same draw from the 2013 absentee ballot bonuses.

BC 2017 Election Simulations, Correlated Case

For the uncorrelated case, there is a 75.4% chance that the result remains unchanged at 43-41 for the BC Liberals over the NDP. About 97 percent of these are cases when no districts flipped; 3 percent are cases when the NDP gains canceled out the BC Liberal gains. So, by far the most likely outcome is no change.

However, there is still a 24.6% chance that something will change. in 11.6% of the cases, the new result is a BC Liberal majority with 44 seats. About 85 percent of these are times when Courtenay-Comox flips; 15 percent are times when Maple-Ridge Mission flips. There is also a small chance that the BC Liberals can take both Courtenay-Comox and Maple-Ridge Mission to form a slightly-more solid majority at 45-39.

Given that the NDP lead in Courtenay-Comox is only 9 votes, why is it so rare that the BC Liberals flip it? The answer is that in 2013 it was quite rare for the BC Liberals to increase their vote share with their absentee ballot bonus. Only 11 of 85 seats in 2013 saw the BC Liberal vote share grow between the preliminary and final counts. So, a 9 vote lead may be small, but the BC Liberals rarely make any gains so it may just be too much to overcome.

On the NDP side, there is a 12.3% chance that they gain a seat. This would lead to a 42-42 tie with the BC Liberals. The most likely candidate is Coquitlam-Burke Mountain, where the current deficit is now 268 votes. There is about a 9 percent chance this flips to the NDP. While it would be more of a stretch, there is still about a 6 percent chance the NDP could make up the 263 vote margin in Richmond-Queensborough. There is a very small chance that the NDP swings both seats to take a 43-41 lead. In the uncorrelated case, this probability is 0.5%, but in the correlated case this probability rises to 5.9%. This bigger chance in the correlated case happens because if the NDP happens to get a lucky draw, that lucky draw swings all their ridings. In contrast, with the uncorrelated case they need two lucky draws at the same time to swing two seats at the same time.

It is very unlikely that the NDP can attain the 44 seats necessary to reach majority status. To do so, they’d need to flip Vancouver-False Creek where they face a 560 vote (2.6%) deficit. There is no precedent from 2013 for a swing this big for the NDP. However, it is not impossible–the NDP could conceivably generate a swing larger than any they enjoyed in 2013. While not impossible, I judge this very unlikely. So, the ceiling for the BC NDP is almost surely 43 seats.

Conclusion

This blog post aims to provide a sense of the potential volatility of the final results in the 2017 BC election. Because around 10 percent of ballots are yet to be counted, up to four electoral districts may flip from one party to another when the final count is announced between May 22nd and May 24th. While the most likely scenario is no change to the status quo 43-41-3 seat count, there is about a 25 percent chance that the seat count will change.

Whatever scenario is presented to us with the Final Count at the end of May, the new legislature will be volatile. See David Moscrop in Maclean’s or Jason Markusoff (also in Maclean’s) for informative discussions of the various scenarios and how they might work.

I’m going to offer some brief comments on US tax reform in three parts: a Premise, a Model, and some Implications.

Premise

In my reading of the legislative situation in the US, the most likely scenario in the US is a temporary (3-5 year) CIT rate cut. I say temporary for 5 reasons:

I don’t think permanent structural reform is likely.

A deficit-financed tax cut won’t get 60 votes in the Senate, so will be capped at 10 years

Rate cuts are easy to reverse; no big inter-industry lobbying and squabbling. It can just happen.

Democrats may be in power again before we get too deep into 2020s.

US federal long-run finances may force even the GOP to raise taxes in 2020s.

I don’t claim to have a legislative crystal ball, so if you think another scenario is more likely then you are free to do so. But for my comments here I will think through the implications of a temporary rate cut in the US.

The Model

The model I have in mind is one where firms make long-run investment decisions based on the long-run after-tax cost of capital. The temporary tax cut can be analyzed using the model of Jack Mintz (World Bank Economic Review 1990) on corporate tax holidays.

Mintz showed that when a firm receives a tax holiday, the impact on long-run investment depends critically on the timing of the realization of income and depreciation/interest deductions. Under a tax holiday, deductions are much more valuable later on when taxes go back up, while income is better when realized early during the holiday period.

Implications

I see 5 implications of the tax holiday model for the US temporary tax cut scenario.

Impact on long-run investment depends on magnitude and expected duration of any tax cut. Small and short? Deep and extended?

Less investment in assets with accelerated depreciation; more in ones with deferred depreciation. In the holiday model, firms want income now and deductions later. (IP? LBOs of firms in mature industries? Other examples?)

Repatriation of accumulated US overseas retained earnings during holiday period–not quite a full tax amnesty, but will have an impact. Can mean temporary positive revenue effects for US Treasury.

If US tax disadvantage shrinks, less investment in new income-shifting/BEPS transactions and infrastructure. But remember BEPS activity is to some extent a knife’s edge thing: existing tax infrastructure (eg Burger King HQ in Mississauga) would only reverse if US gets its rates below those in other countries.

Canada’s concern in matching any US policy action should be proportional to the expected depth and duration of the tax holiday because of long-run investment, and our concern should rise disproportionately if the US gets its statutory combined (fed+prov/state) rate beneath Canada’s because of BEPS.

From September 1, 2016 to December 31, 2016 I will spend 80 percent of my time working for Finance Canada under an Interchange Agreement. This is similar to a ‘secondment‘; Finance Canada is paying UBC an amount equal to 80 percent of my regular UBC salary for those four months.

My work during those four months will consist of some special research projects directed by Finance, regular consultations with Finance staff, and meetings of the full panel of experts advising the Finance review of federal tax expenditures. This work will mostly take place in Vancouver, with some trips to Ottawa.

My UBC work during this time will consist of some continuing administrative duties, advising of graduate students, and other academic activities.

During the course of this agreement, I am contractually committed to refraining from making “through any public medium, either directly or through a third party, any statement critical of Finance Canada or government policies, programs, or officials, or on matters of current political controversy where the statements or actions might create a conflict with the duties of his position or Finance Canada’s and the Government of Canada’s programs and policies.” So, I will be limiting my contact with the public and the media (including my Twitter account) during this period.

I will return to full-time UBC work on January 1st, 2017.

Professor Kevin Milligan, UBC Vancouver School of Economics

Draft Comments to House of Commons Finance Committee

Delivered by Videoconference

April 14, 2016

Noon EDT / 9am PDT

Thank you for the invitation to comment on Bill C-2. I would like to make two brief points on the new 33% tax bracket and its impact on tax planning and avoidance.

First, I’d like to emphasize the importance of the federal-provincial angle. In a federation like Canada, it is more difficult to tax mobile economic factors at the provincial level. For example, if a province tries to tax high earners, some of that income may shift to other provinces through use of financial and accounting techniques—an example is the Alberta Family Trust into which a high-earner from another province can shift assets that are then taxed at Alberta’s lower rates.

On the other hand, at the federal level it is harder to avoid taxation because shifting income out of the country is harder than shifting between provinces within the country.

In research with Michael Smart from the University of Toronto, we found that high-income taxpayers are much less likely to shift their income in response to a federal tax change than they are to a provincial tax change. So, when looking at the revenue implications of a new high income tax bracket, the revenue expectations at the federal level should be higher than at the provincial level.

My second point is that enhanced administrative measures are critical to combat tax planning and avoidance. If the CRA makes it harder for individuals to engage in tax planning, the new 33% bracket is more likely to reach its revenue targets.

The government has already announced several measures that move in that direction, including a change in the recent budget in the definition of active vs. passive income for small-business corporations and also new enforcement programs to be introduced by the CRA.

But I believe there is still more to do.

Reduce use of small business corporations as tax shelters: examine spousal dividends and the lifetime capital gains exemption, and consider an employee count or hours threshold, as Quebec has done.

Re-open the case for the taxation of stock options.

On the international front, organizations like the OECD pursue multilateral agreements to curb tax planning and tax avoidance at the corporate and individual level. Canada should be taking a leadership role in pushing these processes forward.

Canada deserves a tax system that is fair. I believe the steps taken over the past few months have been mostly in the right direction, but there remains work to be done.