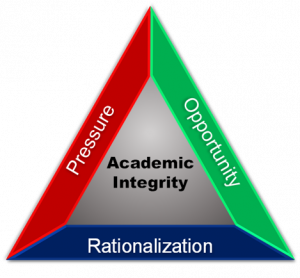

One model of academic dishonesty is based on what is commonly known as the Fraud Triangle; it argues that the presence of three elements (pressure, opportunity, and rationalization) each increase the likelihood of academic misconduct. This can be a powerful framework for instructors designing courses and assessments in large part because it combines both root causes and preventions for misconduct. To avoid the negative and accusatory connotations of “fraud,” the model on this page has been adapted to positive, growth-oriented phrasing under the name Academic Integrity Triad.

An instructor can enhance academic integrity by first recognizing each dimension of the Triad:

- Pressure: academic and other pressures on students work against the goal of fostering academic integrity. Pressure can come from real or perceived requirements to pass or to achieve high grades. These pressures can be internal (from the student) or external (e.g. from maintaining scholarship or visa requirements; from meeting requirements for entrance to programs or co-op; or from satisfying parents). Pressure can also come from peers, such as in requests for help or following along with what others are doing. In many cases, pressure may cause students to behave in ways they would not otherwise (i.e., “panic cheating”), and issues of pressure are exacerbated as student stress increases and wellbeing diminishes.

- Opportunity: opportunity refers to making academic integrity the easy choice for students, in light of all of the pressures they are facing. Relatively speaking, this means seeking ways to make engaging in academically dishonest behaviours more difficult than engaging in honest ones. Practically this is done through the presence or barriers to misconduct and mechanisms to detect and address misconduct if it happens.

- Rationalization: rationalization is shown as the foundation to the triad above as it is also the foundation to academic integrity. Rationalization refers to ensuring students both understand and value academic integrity such that they choose a path of integrity even when pressures are high and barriers to academic misconduct are not present. Rationalizing academic integrity becomes easier for a student when they have clear guidance in terms of what behaviours are acceptable and expected, and when they perceived that violations of academic integrity are taken seriously and dealt with appropriately. A perception that other students are engaging in and getting away with dishonest behaviours makes it more difficult to rationalize integrity. In many ways, the key element of rationalization comes down to a student being able to make a choice that the risks and costs (both personal and external) are not worth any potential rewards of dishonest behaviour.

|

An analogy As an analogy, think of a driver of an automobile who is supposed to be somewhere but is running late, and how the following might affect whether they exceed the speed limit. If they are driving to a friend’s house for a casual visit there is less pressure to arrive at a particular time (and less pressure to speed) than if they are rushing to catch a flight at the airport. If the road they are on uses traffic calming measures (such as roundabouts, narrowed lanes, and speed humps), there is less opportunity to speed. Finally, if school zones, bike lanes, and pedestrian crossings are well marked, and if drivers understand that fatality rates on roads drop dramatically with lower speed, it is easier for a driver to rationalize traveling at the speed limit. This analogy can be extended to academic misconduct in several ways, introduced here and left for you to ponder. There are standard speed limits in a city and care goes into training new drivers about this; any deviations from the standards are clearly identified at the point where that information is needed (i.e., speed limits are posted). A driver’s decision-making can be clouded in the moment when pressure is high; for the driver about to miss their flight, at that instant, getting to the airport on time might seem like the most important thing in the world. Most drivers are influenced by what they see other drivers around them doing; a driver is more likely to speed if it seems all other drivers on the road are speeding too. Conversely, a driver is more likely to travel the speed limit if they see all other drivers doing the same. Police can control speeding behaviour through enforcement, such as by issuing speeding tickets; however, this can have unintended consequences such as suggesting the reason to follow the speed limit is to avoid getting a ticket, which in turn suggests speeding is not as bad when the police are not around. A comprehensive strategy to reduce speeding that addresses all three of pressure, opportunity, and rationalization is more likely to be successful than any strategy reliant on a single element. |

Choo and Tan [1] found that the absence of any one of the three elements of the Academic Integrity Triad (i.e., there was high pressure on students, students had the opportunity to cheat without being caught, or students were able to rationalize cheating) led to a statistically significant increase in cheating behaviours. They also found interaction effects: from a baseline propensity to cheat of approximately 20%, when none of the three elements were addressed this climbed to 33%. When all of the elements were addressed (i.e., measures were taken to reduce pressure, opportunity, and the ability to rationalize cheating), the likelihood of cheating dropped to 8%.

We can impact all three elements in our assessment and course design, and reduce the likelihood of misconduct as discussed on the strategies for promoting academic integrity page.

References

- Freddie Choo and Kim Tan, The effect of fraud triangle factors on students’ cheating behaviors, Advances in Accounting Education: Teaching and Curriculum Innovations, Volume 9, 205–220, 2008, ISSN: 1085-4622/doi:10.1016/S1085-4622(08)09009-3

| Previous (Misconduct by the Numbers) | Next (Enhancing Academic Integrity) |