Three Definitions Assignment

The use of professional terms can provide clarity and meaning, or leave people confused. The goal of technical writing is clarity. Providing a definition at the appropriate level for the intended audience and situation can provide transparency and a common language. Failure to reach an understanding can lead to confusion, misunderstanding and ultimately legal challenges. Definitions should be brief and direct, as well as matching the audience’s knowledge level in the given subject area.

The purpose of this assignment is to provide three different definitions for the same term: a parenthetical definition, a sentence definition and an expanded definition. The level of language used in these definitions should match the identified situation and audience.

Situation/audience: I am an accountant working at an accounting firm. A potential client has come to the office for an initial meeting after inheriting a small business. Their knowledge of financial bookkeeping/accounting is sparse. We will examine the company’s assets and liabilities to determine the company’s equity as represented on a balance sheet (ledger of liabilities, assets and equity, kept in the form of double-entry bookkeeping).

BALANCE SHEET

A balance sheet is a financial statement used by accountants and bookkeepers to determine the equity or the value of an owner or shareholder’s interest in a company. Equity is determined by subtracting a company’s liabilities (everything a company owes) from a company’s assets (economic resources). On the balance sheet, assets and liabilities/equity are listed on opposite sides and the items in the categories are listed based on liquidity*. This is known as double-entry bookkeeping.

History

Accounting terms stated to emerge in the 14th and 15th century. The first balance sheet was published in 1494 by Franciscan monk Luca Pacioli. It listed an entity’s resources (credits) separate from any claim upon those resources (debts). (Peterka) This was the first record of double-entry bookkeeping and it led to the equation we know today as:

Assets = Liabilities + Owners’ Equity.

Europeans migrating to America brought this new system with them and as corporations grew this bookkeeping evolved into modern day accounting. The construction of the railway sped up the rate at which business transactions were performed requiring a more sophisticated record keeping system. Eventually balance sheets were published for larger companies as they tried to attract more capital for further expansion. The robust equation helped business owners, workers and investors make smarter decisions on the state of a business’s financials.

Analysis of parts

To get a better understanding of a balance sheet it is important for us to look at the parts.

Assets

Assets represent what the company owns. They have some economic benefit to the company and the company has control over that benefit resulting from a past transaction or event. Assets can take the form of cash, inventory, property (and other fixed assets*), or accounts receivable.

Contracts may also represent assets. A patent purchased by the company has value because it gives the owner access to future cash flows from the sale of the patented product. Another example of an asset generated through contractual rights is a leased machine. The lease contract gives the company contractual rights to use the asset even though the company does not have legal title to the machine.

Liabilities

Liabilities represent what the company owes. They have a negative economic value and require the company to give up assets to settle the obligation. Liabilities include rent, wages, utilities, loans, and accounts payable* and may be accrued by:

- contractual obligations such as an employee who needs to be paid for services rendered or they will quit or sue the company.

- Statutory obligations such as illegally polluting.

- Contingent obligations which arise through past or present practice that signal that the company acknowledges a potential economic burden. An example would be a company who said the stand behind their products. A defective product does not require replacement due to terms of service but the company policy of standing behind their product laves the expectation that they will replace it or face a lawsuit.

- Equitable obligations arise due to ethical or moral considerations. An example would be a company’s moral obligation to retrain an employee who is being downsized.

Equity

Equity is the owner or shareholder’s interest in the company. It is determined by subtracting a company’s liabilities from a company’s assets. It is also referred to as a company’s net worth. If the business were sold, this would be its residual value.

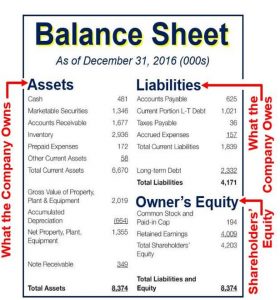

Balance Sheet Example

As you can see in the example below, all assets are listed in the left-hand column and then totaled at the bottom. All Liabilities are listed in the right-hand column and then totaled. Below the liabilities total the equity is itemized and totaled. The purpose of a balance sheet and double-entry bookkeeping is that, if done correctly, both columns should have the same total. The total for assets should equal the total for liabilities + owner’s equity. If these two do not balance, then something has been missed.

(Peterka)

Frequently Asked Questions

How does it work?

A balance sheet is made up of three parts: assets, liabilities and owner/stakeholder equity. Equity is determined by subtracting a company’s liabilities from the company’s assets. What you are left with is the company’s equity. This is all represented on a balance sheet, aptly called since if calculated correctly the equity should balance with the assets minus the liabilities as represented in the graphic below.

(Nikolaev)

How is it differentiated?

Unlike other forms of bookkeeping where items are entered a single time in a log arranged in chronological order, balance sheets follow the principal of double entry. In doing so there is an internal check built into balance sheets which does not exist in traditional single-entry bookkeeping. On balance sheets, both columns must equal the same number. If they do not, then the bookkeeper knows there is an error or missing information, prompting them to check their work.

____________________________________________________________________________________________________________________________________________________________________

Glossary

Fixed asset – A tanglible capital assets that are acquired for use in the business and are not for resale, are long term in nature and are usually subject to depreciation.

Liquidity – A company’s ability to convert assets into cash to pay off is current liabilities.

____________________________________________________________________________________________________________________________________________________________________________________

References

“Assets, Liabilities, Equity – The Building Blocks of a Company.” Investor Academy, 27 May 2016, investoracademy.org/assets-liabilities-equity-building-blocks-of-company/.

Hayes, Adam. “Balance Sheet.” Investopedia, Investopedia, 13 May 2020, www.investopedia.com/terms/b/balancesheet.asp.

Horngren, Charles T., et al. Accounting. 9th ed., vol. 1, Pearson, 2014.

Kieso, Doanld E., et al. INTERMEDIATE ACCOUNTING. JOHN WILEY & Sons, 2016.

Lannon, John M., and Laura J. Gurak. Technical Communication. 14th ed., Pearson, 2018.

Liabilities – Balance Sheet Definition, www.free-management-ebooks.com/faqfi/balance-04.htm.

Nikolaev, Kiril. “Assets, Liabilities, Equity – The Building Blocks of a Company.” Investor Academy, 27 May 2016, investoracademy.org/assets-liabilities-equity-building-blocks-of-company/.

Peterka, Bruce. “The History of the Balance Sheet – Blog for Accounting & QuickBooks Tips – Peak Advisers Denver.” Peak Advisers, Peak Advisers, 21 Dec. 2017, www.peakadvisers.com/blog/2017/12/21/the-history-of-the-balance-sheet.

Leave a Reply